Student Loan Repayment 2026: Federal Program Updates & 10% Savings

The landscape of student loan repayment is constantly evolving, and for borrowers looking ahead to 2026, understanding the upcoming federal program updates is paramount. With potential shifts in policy and new opportunities for savings, staying informed can make a significant difference in your financial well-being. This comprehensive guide will delve into the anticipated changes, highlight strategies to potentially save 10% or more on your payments, and equip you with the knowledge to navigate your student loan obligations effectively in 2026 and beyond. Our focus is squarely on the crucial aspects of student loan 2026, ensuring you have the most up-to-date and relevant information at your fingertips.

For millions of Americans, student loans represent a substantial financial commitment. The federal government, recognizing the burden this can place on individuals, frequently reviews and adjusts its repayment programs. These adjustments are not merely bureaucratic formalities; they can have a direct and profound impact on your monthly budget, the total amount you repay, and your overall financial trajectory. As we approach 2026, several key areas of federal student loan policy are expected to see significant developments, offering both challenges and opportunities for borrowers. Understanding these nuances is the first step toward optimizing your repayment strategy.

Understanding the Current Student Loan Repayment Landscape

Before we dive into the specifics of student loan 2026, it’s essential to have a firm grasp of the current federal student loan repayment options. The existing framework offers a variety of plans designed to accommodate different financial situations, from standard repayment to income-driven repayment (IDR) plans. Each plan has its own set of rules, eligibility criteria, and implications for interest accrual and potential forgiveness.

Standard Repayment Plan

The Standard Repayment Plan is the default option for most federal student loans. Under this plan, borrowers make fixed monthly payments for up to 10 years (or up to 30 years for consolidated loans). While it typically results in the lowest total interest paid over the life of the loan, the monthly payments can be substantial, especially for those with high loan balances or lower incomes. It’s a straightforward approach but may not be suitable for everyone.

Graduated Repayment Plan

The Graduated Repayment Plan starts with lower payments that gradually increase over time, typically every two years. The repayment period is still up to 10 years. This plan can be appealing to borrowers who expect their income to rise, as it provides some relief in the initial years. However, because payments start lower, more interest accrues in the early stages, meaning you might pay more overall compared to the Standard Plan.

Extended Repayment Plan

For borrowers with more than $30,000 in federal student loan debt, the Extended Repayment Plan offers a longer repayment period of up to 25 years. Payments can be fixed or graduated. This plan significantly lowers monthly payments, but like the Graduated Plan, it often results in paying more interest over the loan’s lifetime. It’s a useful option for those needing to reduce their monthly financial burden.

Income-Driven Repayment (IDR) Plans

Income-Driven Repayment (IDR) plans are perhaps the most flexible and complex options available. These plans calculate your monthly payment based on your income, family size, and federal poverty guidelines. The goal is to make payments more affordable, typically capping them at a percentage of your discretionary income. After a certain period (20 or 25 years, depending on the plan), any remaining balance may be forgiven, though this forgiven amount is often considered taxable income.

Current IDR plans include:

- Income-Based Repayment (IBR): Payments are generally 10% or 15% of your discretionary income, depending on when you took out your loans.

- Pay As You Earn (PAYE): Payments are typically 10% of your discretionary income, but never more than what you would pay under the Standard Repayment Plan.

- Revised Pay As You Earn (REPAYE): Payments are generally 10% of your discretionary income, regardless of when you took out your loans. This plan has been largely replaced by the new SAVE plan for new enrollees.

- Income-Contingent Repayment (ICR): Payments are either 20% of your discretionary income or what you’d pay on a fixed 12-year plan, whichever is less. This is the only IDR plan available for Parent PLUS loans (after consolidation).

Understanding these existing plans forms the foundation for appreciating the significance of upcoming changes for student loan 2026. Many of the new developments aim to refine and improve upon these existing frameworks, particularly the IDR options.

Key Federal Program Updates for Student Loan 2026

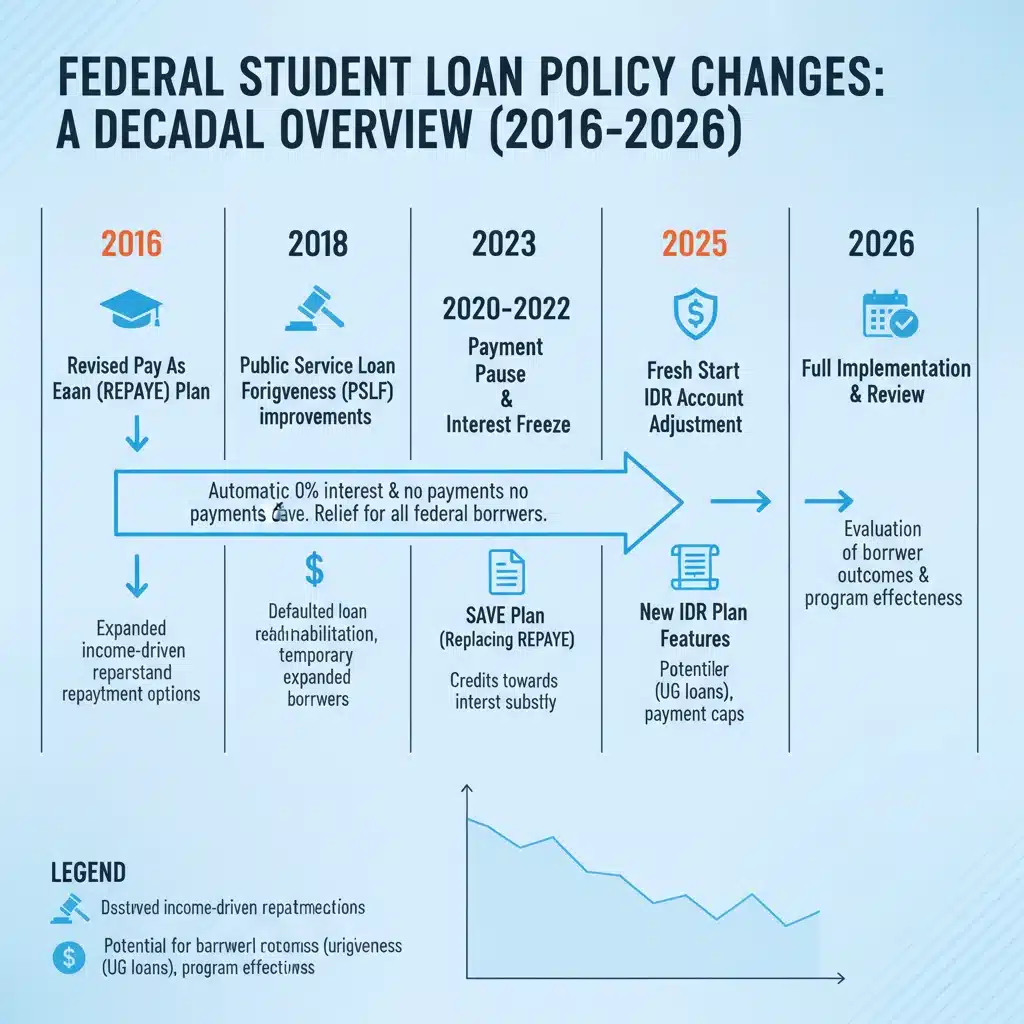

As we look towards 2026, several federal program updates are either already in motion or anticipated to take full effect, significantly reshaping the student loan repayment landscape. The most prominent of these is the continued rollout and full implementation of the Saving on a Valuable Education (SAVE) Plan, which replaces the REPAYE plan and offers potentially substantial benefits to borrowers.

The SAVE Plan: A Game Changer for Borrowers

The SAVE Plan, which began rolling out in 2023, is designed to be the most affordable income-driven repayment plan to date. By 2026, its full benefits are expected to be widely implemented, offering significant relief to many borrowers. Here’s a breakdown of its key features and how they impact student loan 2026:

- Reduced Discretionary Income Calculation: Under SAVE, the amount of income considered ‘discretionary’ is significantly higher than in previous IDR plans. Instead of 150% of the poverty line, SAVE protects 225% of the poverty line from being counted towards your discretionary income. This means more of your income is excluded from the payment calculation, leading to lower monthly payments for many.

- Lower Payment Percentage: For undergraduate loans, monthly payments under SAVE will be calculated at 5% of your discretionary income, down from 10% or 15% in other IDR plans. For graduate loans, the rate is 10%. Borrowers with both undergraduate and graduate loans will pay a weighted average. This is a crucial area where borrowers can potentially see a 10% or more reduction in their monthly outlay compared to older IDR plans.

- Interest Subsidy: One of the most impactful features of the SAVE Plan is its interest subsidy. If your calculated monthly payment doesn’t cover the monthly interest, the government will cover the remaining interest. This prevents your loan balance from growing due to unpaid interest, a common frustration for borrowers on other IDR plans. This provision alone can save borrowers thousands of dollars over the life of their loan and is a major improvement for student loan 2026 planning.

- Shorter Path to Forgiveness: For borrowers with original loan balances of $12,000 or less, the SAVE Plan offers loan forgiveness after just 10 years of payments, significantly shorter than the 20 or 25 years typically required by other IDR plans. For every $1,000 borrowed above $12,000, an additional year of payments is added, up to the standard 20 or 25 years.

- Automatic Enrollment Option: While not fully implemented for all borrowers yet, there are discussions and pilot programs for automatic enrollment into the most beneficial IDR plan (often SAVE) for eligible borrowers, streamlining the process and reducing administrative hurdles.

The SAVE Plan is a cornerstone of the federal government’s efforts to make student loan repayment more manageable and equitable. Its full implementation by 2026 will be a critical development for millions of borrowers, offering a clear path to lower payments and preventing balance growth.

Other Potential Policy Changes and Considerations

Beyond the SAVE Plan, other policy discussions and potential changes could impact student loan 2026. These include:

- Public Service Loan Forgiveness (PSLF) Enhancements: While significant reforms to PSLF have already been implemented, ongoing efforts aim to simplify the process and ensure more eligible public servants receive the forgiveness they’ve earned. Borrowers should continue to monitor updates regarding PSLF, especially concerning qualifying payments and employer verification.

- Consolidation Rules: The rules around loan consolidation, particularly for older FFEL Program loans and Perkins Loans, may continue to evolve. Consolidating these loans into a Direct Consolidation Loan is often necessary to access federal benefits like IDR plans and PSLF. Borrowers with older loan types should pay close attention to any deadlines or windows of opportunity for consolidation.

- Tax Implications of Forgiveness: Currently, most federal student loan forgiveness under IDR plans is considered taxable income by the IRS, with an exception for forgiveness granted between 2021 and 2025. What happens beyond 2025 remains a critical question. Borrowers planning for forgiveness in 2026 or later should consult with a tax professional to understand potential tax liabilities.

- Interest Rate Changes: While not a program update per se, federal student loan interest rates are set annually based on market conditions. Borrowers should be aware that new loans issued in 2026 will have rates determined by the prevailing market at that time, which can influence future borrowing decisions. Existing loan interest rates are fixed.

Staying abreast of these potential changes is vital. The federal student aid website (StudentAid.gov) is the official source for all updates and should be regularly consulted.

Strategies to Potentially Save 10% on Your Student Loan 2026 Payments

With the federal program updates, particularly the SAVE Plan, there are concrete strategies you can employ to potentially reduce your monthly student loan payments by 10% or more in 2026. The key lies in understanding your eligibility and proactively taking steps to optimize your repayment plan.

1. Enroll in the SAVE Plan (or Re-Evaluate if Already Enrolled)

This is arguably the most impactful strategy for many borrowers. If you are currently on the REPAYE plan, you will automatically be transitioned to the SAVE Plan. However, if you are on another IDR plan (IBR, PAYE, ICR) or the Standard/Graduated/Extended plans, you will need to actively switch to SAVE to reap its benefits. Evaluate your current payment against what your payment would be under SAVE. The reduced discretionary income calculation and the 5% payment rate for undergraduate loans are the primary drivers of savings here. For many, this switch alone could lead to a significant reduction, easily exceeding 10%.

Actionable Steps:

- Visit StudentAid.gov.

- Log in to your account and navigate to the ‘Repayment’ section.

- Use the Loan Simulator tool to compare your current plan with the SAVE Plan.

- Apply for the SAVE Plan if it offers a lower payment. Be prepared to provide income and family size documentation.

2. Understand the Interest Subsidy and Prevent Balance Growth

The SAVE Plan’s interest subsidy is a hidden gem for savings. While it doesn’t directly reduce your monthly payment amount, it prevents your loan balance from ballooning due to unpaid interest. If your monthly payment is $0 or very low, but your interest accrues at a higher rate, the government will cover the difference. This means you’re not digging yourself into a deeper hole. Over the long term, preventing this balance growth is a form of significant saving, as it reduces the total amount you’ll eventually repay.

Actionable Steps:

- Ensure you are on the SAVE Plan.

- Monitor your loan balance regularly through your loan servicer’s portal to confirm interest isn’t accumulating.

3. Re-Certify Your Income Annually (or When Your Income Decreases)

For all IDR plans, including SAVE, you are required to re-certify your income and family size annually. This is a critical opportunity to ensure your payments accurately reflect your current financial situation. If your income has decreased since your last certification, re-certifying immediately (rather than waiting for the annual due date) can lead to a lower payment. Conversely, if your income has increased significantly, re-certifying might lead to a higher payment, but failing to re-certify can sometimes lead to capitalization of interest, which you want to avoid.

Actionable Steps:

- Mark your calendar for your annual re-certification date.

- If you experience a significant income drop, apply for re-certification as soon as possible.

- Keep accurate records of your income and family size documentation.

4. Consider Loan Consolidation for Access to Better Plans

If you have older federal student loans, such as Federal Family Education Loan (FFEL) Program loans or Federal Perkins Loans, you might not be eligible for the SAVE Plan or PSLF directly. Consolidating these loans into a Direct Consolidation Loan can make them eligible for these beneficial programs. While consolidation doesn’t necessarily lower your interest rate (it takes a weighted average of your existing rates), it can unlock access to plans that dramatically reduce your monthly payments, potentially saving you more than 10%.

Actionable Steps:

- Identify your loan types by logging into StudentAid.gov.

- If you have FFEL or Perkins loans, research the Direct Consolidation Loan process.

- Consider consolidating if it opens access to the SAVE Plan or PSLF.

5. Explore Public Service Loan Forgiveness (PSLF)

If you work for a qualifying government or non-profit organization, PSLF can lead to the forgiveness of your remaining federal student loan balance after 120 qualifying monthly payments (10 years). Payments made under the SAVE Plan (and other IDR plans) typically count towards PSLF. While not a direct 10% monthly saving, the complete forgiveness of your remaining balance can represent an astronomical saving over the life of your loan, far exceeding 10% of your total debt.

Actionable Steps:

- Verify if your employer qualifies for PSLF using the PSLF Help Tool on StudentAid.gov.

- Submit an Employment Certification Form (ECF) annually or whenever you change employers to track your qualifying payments.

- Ensure you are on a qualifying repayment plan, such as the SAVE Plan.

6. Strategic Use of Payments During Grace Periods or Deferment

While not directly related to federal program updates for student loan 2026, optimizing your payments during grace periods or deferment can lead to long-term savings. If you can afford to make interest-only payments during periods of deferment or your grace period, it can prevent that interest from capitalizing (being added to your principal balance), thereby reducing the total amount you’ll pay interest on.

Actionable Steps:

- If you are in a grace period or deferment, check if interest is accruing.

- If affordable, make interest-only payments to prevent capitalization.

7. Monitor for Legislative Changes

The student loan landscape is dynamic. While the SAVE Plan is a significant step, future legislative actions could introduce new programs, modify existing ones, or address issues like the taxability of forgiven debt. Staying informed through official government channels and reputable financial news sources is crucial.

Actionable Steps:

- Subscribe to email updates from StudentAid.gov.

- Follow reliable financial news outlets that cover student loan policy.

Who Benefits Most from the Student Loan 2026 Updates?

The federal program updates, particularly the SAVE Plan, are designed to benefit a broad range of borrowers, but some groups will experience more significant positive impacts than others as we move into student loan 2026.

- Low- and Middle-Income Borrowers: Those with lower incomes, especially relative to their loan balances, will see the most substantial reductions in monthly payments due to the expanded discretionary income protection and the 5% payment rate for undergraduate loans. Many could have $0 monthly payments.

- Borrowers with Undergraduate Loans: The 5% payment rate on undergraduate loans is a significant advantage. Borrowers with only undergraduate debt or a higher proportion of undergraduate debt will likely see greater savings.

- Borrowers with Growing Balances: The interest subsidy feature of the SAVE Plan is a lifeline for borrowers whose payments don’t cover accruing interest. This prevents their loan balances from growing, offering long-term financial stability.

- Public Service Workers: While PSLF is a separate program, the SAVE Plan’s affordable payments and interest subsidy make it an ideal companion for those pursuing PSLF, ensuring their payments count towards forgiveness without their balance increasing.

- Borrowers with Small Loan Balances: The accelerated forgiveness timeline (10 years for balances of $12,000 or less) under SAVE is a huge boon for those with smaller debts, offering a quicker path to debt freedom.

Conversely, borrowers with very high incomes relative to their debt, or those who were already comfortable with the Standard Repayment Plan, might not see significant changes or benefits from these particular updates, as their payments might not be reduced further. However, the interest subsidy still offers a safety net for everyone on SAVE.

Potential Challenges and What to Watch For

While the outlook for student loan 2026 includes many positive changes, it’s also important to be aware of potential challenges and areas that require careful attention:

- Administrative Hurdles: Large-scale program changes can sometimes lead to administrative delays or confusion. Borrowers should remain proactive in checking their loan servicer accounts and communicating any discrepancies.

- Communication Gaps: Ensure you are receiving official communications from your loan servicer and the Department of Education. Update your contact information to avoid missing critical updates or re-certification notices.

- Taxability of Forgiven Amounts (Post-2025): As mentioned, the tax treatment of forgiven student loan debt after 2025 is uncertain. This will be a significant factor for borrowers nearing their forgiveness timeline. Seek professional tax advice.

- Future Legislative Changes: The political landscape can shift, and with it, federal student loan policies. While the SAVE Plan is a current federal initiative, future administrations or congressional actions could modify or introduce new policies. Staying informed is your best defense.

- Private Student Loans: It’s crucial to remember that these federal program updates only apply to federal student loans. Private student loans operate under different rules and do not qualify for federal IDR plans or forgiveness programs. If you have private loans, you’ll need to explore separate refinancing or repayment options with your private lender.

Making the Most of Your Student Loan 2026 Repayment

To effectively manage your student loan 2026 repayment, a proactive and informed approach is essential. Here’s a summary of best practices:

- Stay Informed: Regularly check StudentAid.gov for the latest official updates, FAQs, and policy changes.

- Know Your Loans: Understand whether your loans are federal or private, and what types of federal loans you have (Direct, FFEL, Perkins). This determines your eligibility for various programs.

- Utilize the Loan Simulator: This free tool on StudentAid.gov is invaluable for comparing repayment plans and estimating your monthly payments under different scenarios, including the SAVE Plan.

- Communicate with Your Servicer: If you have questions, need to update information, or are facing financial hardship, contact your loan servicer. They are your primary point of contact for managing your loans.

- Re-certify On Time: If you’re on an IDR plan, timely annual re-certification of your income and family size is critical to maintain your payment level and avoid interest capitalization.

- Build an Emergency Fund: Having a financial cushion can provide peace of mind and prevent you from missing payments if unexpected expenses arise.

- Consider Professional Advice: For complex situations, a certified financial planner or student loan expert can offer personalized guidance.

The year 2026 holds significant promise for federal student loan borrowers, primarily due to the full implementation of the SAVE Plan. This plan, with its enhanced discretionary income protection, lower payment percentages, and crucial interest subsidy, offers a tangible path to more affordable payments and preventing runaway interest. By actively engaging with these updates, understanding your options, and taking proactive steps, you can position yourself to potentially save 10% or more on your monthly payments and achieve greater financial stability.

Navigating student loan repayment can feel daunting, but with the right information and strategy, it becomes a manageable challenge. Embrace the opportunities presented by the student loan 2026 federal program updates, and take control of your financial future.