New Homebuyer Tax Credits 2026: Claim Up to $8,000 Federal Incentives

Are you dreaming of owning a home in 2026? The prospect of stepping onto your own property, painting the walls your favorite color, and building equity can be incredibly exciting. However, the financial hurdles often seem daunting. The good news is that the federal government is introducing new homebuyer tax credits for 2026, designed to make homeownership more accessible and affordable. These significant incentives could provide eligible individuals and families with up to $8,000, offering a substantial boost to your home-buying journey. Understanding these new homebuyer tax credits is crucial for anyone planning to purchase a home in the coming year, as they can dramatically reduce your out-of-pocket expenses and overall financial burden.

Navigating the world of real estate and government incentives can be complex, but with the right information, you can strategically leverage these programs to your advantage. This comprehensive guide will delve into everything you need to know about the 2026 homebuyer tax credits, from eligibility requirements and application processes to maximizing your benefits. We’ll break down the nuances, offer practical advice, and help you prepare to claim your share of these valuable federal incentives. Whether you’re a first-time homebuyer or looking to re-enter the housing market, these new homebuyer tax credits could be the key to unlocking your homeownership dreams.

Understanding the New Homebuyer Tax Credits for 2026

The federal government periodically introduces or modifies tax incentives to stimulate economic activity, particularly in sectors like housing. The new homebuyer tax credits for 2026 are a testament to this ongoing commitment, aiming to support individuals and families in achieving homeownership. These credits are not merely deductions; they are direct reductions in the amount of tax you owe, dollar for dollar. This means that if you qualify for an $8,000 credit, your tax liability will decrease by $8,000, which can be far more impactful than a deduction that only reduces your taxable income.

At its core, a tax credit is a provision that reduces your federal income tax liability. Unlike tax deductions, which lower your taxable income, tax credits directly subtract from the amount of tax you owe. The 2026 homebuyer tax credits are designed to provide financial relief to eligible homebuyers, effectively lowering the cost of purchasing a home. While the exact legislative details are still being finalized, the proposed structure indicates a significant benefit, potentially up to $8,000, for qualifying individuals. This sum can be a game-changer, covering a substantial portion of closing costs, a down payment, or even contributing to the overall purchase price.

Historically, similar homebuyer tax credits have played a crucial role in stabilizing housing markets and encouraging homeownership, especially during challenging economic times. The 2008 First-Time Homebuyer Tax Credit, for instance, offered up to $8,000 and was instrumental in stimulating the housing market. The new homebuyer tax credits for 2026 are expected to have a similar positive impact, providing a much-needed boost to both aspiring homeowners and the broader economy. It’s important to differentiate these federal credits from state or local programs, though they can often be combined for even greater savings. Always check for local programs that might complement these federal initiatives.

Key Proposed Features of the 2026 Homebuyer Tax Credits

While the final legislation is pending, early indications suggest several key features for the 2026 homebuyer tax credits. These generally include:

- Maximum Benefit: Up to $8,000 for eligible homebuyers. This amount is a direct reduction of your tax liability.

- Eligibility Focus: The credits are primarily targeted at first-time homebuyers, though definitions can vary. Some proposals also include provisions for repeat buyers in specific circumstances, such as those who haven’t owned a home in the past three years.

- Income Limitations: To ensure the credits benefit those who need them most, there will likely be income thresholds. These limits are typically based on a percentage of the area median income (AMI) or a fixed adjusted gross income (AGI) cap.

- Home Purchase Price Limits: The purchased home’s price might be subject to certain limits to ensure the credit supports affordable housing.

- Recapture Provisions: Some past credits included recapture provisions, meaning if you sold the home within a certain period (e.g., 36 months), you might have to repay a portion of the credit. It’s crucial to understand if the 2026 credits will include such clauses.

- Effective Date: The credits are anticipated to be available for homes purchased and closed in 2026.

Staying informed about these proposed features as they evolve into final legislation is paramount. We recommend consulting reputable government sources and financial advisors as the year progresses to get the most accurate and up-to-date information on the new homebuyer tax credits.

Who is Eligible for the $8,000 Federal Incentives?

Eligibility is the cornerstone of claiming any tax credit, and the 2026 homebuyer tax credits are no exception. While the specifics will be outlined in the final legislation, we can anticipate certain criteria based on historical patterns and current discussions. Generally, these credits are designed to assist a broad range of aspiring homeowners, but with specific conditions to ensure equitable distribution and impact.

Defining ‘First-Time Homebuyer’

The term ‘first-time homebuyer’ is often a central component of federal housing incentives. For the purpose of these homebuyer tax credits, a first-time homebuyer is typically defined as an individual who has not owned a principal residence during the two-year period ending on the date of the purchase of the new home. This definition is quite broad and can include individuals who have previously owned property but meet the two-year non-ownership criteria. It’s important to note that if you co-owned a home with a spouse, even if you weren’t on the deed, it might affect your eligibility. Always clarify your specific situation with a tax professional.

Moreover, the credit may extend to individuals who are purchasing a home with a spouse who meets the first-time homebuyer definition, even if the other spouse has previously owned a home. This often comes with specific rules, such as prorating the credit. Keep an eye out for detailed guidance from the IRS once the legislation is passed. The goal is to encourage new entries into the homeownership market, and these homebuyer tax credits are a powerful tool to achieve that.

Income and Purchase Price Limitations

To ensure the homebuyer tax credits are directed towards those who genuinely need assistance, income limitations are almost certainly going to be a factor. These limits prevent high-income earners from claiming the credit, ensuring the funds are distributed to support moderate and middle-income families. Typically, income limits are expressed as a percentage of the area median income (AMI) or as a fixed adjusted gross income (AGI) cap. For example, you might qualify if your income is below 100% or 120% of the AMI for your specific location.

Similarly, there will likely be purchase price limits on the home itself. This ensures that the homebuyer tax credits support the purchase of reasonably priced homes rather than luxury properties. These limits vary significantly by location due to differences in housing costs. It’s crucial to research the specific income and purchase price limits applicable to your area once the final rules for the 2026 homebuyer tax credits are released. These factors are critical in determining your eligibility and the potential amount of credit you can receive.

Other Potential Eligibility Criteria

Beyond the primary definitions, other criteria might influence your eligibility for the 2026 homebuyer tax credits:

- Principal Residence Requirement: The home you purchase must be your primary residence. This means it cannot be an investment property, a vacation home, or a rental property. You must intend to live in the home as your main dwelling.

- Closing Date: The credit will apply to homes purchased and closed within a specific timeframe, likely throughout the 2026 calendar year. The date of closing, not the date of signing a purchase agreement, is usually the determining factor.

- Type of Home: The credit typically applies to single-family homes, townhouses, condominiums, and sometimes even manufactured homes, provided they meet certain criteria and are affixed to a permanent foundation.

- Tax Filing Status: Your tax filing status might also play a role, especially for married couples filing separately.

Staying updated on these specific requirements will be key to successfully claiming the new homebuyer tax credits. Proactive research and consultation with a tax professional can save you a lot of hassle and ensure you don’t miss out on these valuable incentives.

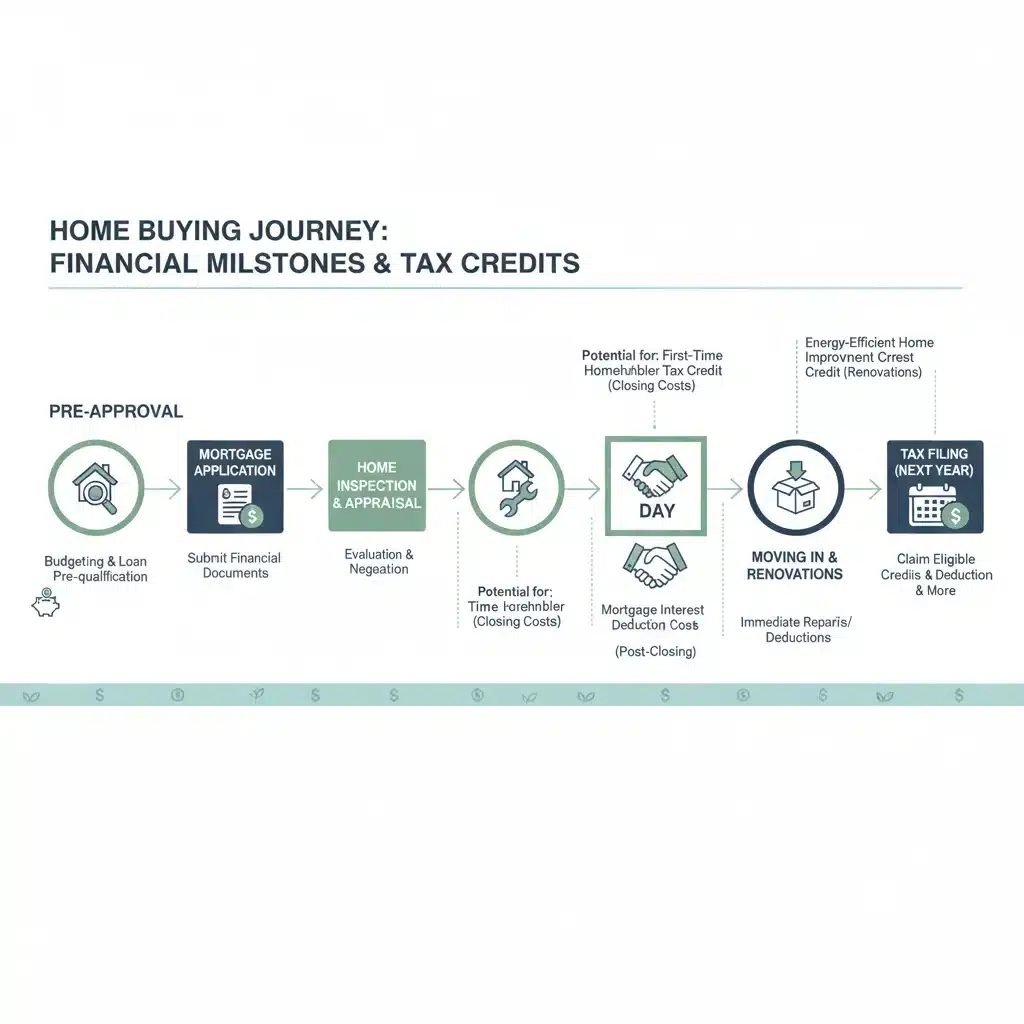

How to Claim the New Homebuyer Tax Credits: A Step-by-Step Guide

Once you’ve determined your eligibility, the next crucial step is understanding how to actually claim the 2026 homebuyer tax credits. The process typically involves careful documentation, accurate tax filing, and potentially working with your mortgage lender. While the exact forms and procedures will be detailed by the IRS, we can outline a general roadmap based on how similar credits have been administered in the past.

Gathering Necessary Documentation

Preparation is key. To successfully claim the homebuyer tax credits, you’ll need to meticulously gather and organize various documents related to your home purchase. This typically includes:

- Settlement Statement (HUD-1 or Closing Disclosure): This document, provided at closing, details all the financial transactions of your home purchase, including the purchase price, closing costs, and other relevant figures. It’s vital for verifying your home purchase.

- Mortgage Documents: Your loan agreements and related paperwork will confirm your financing details.

- Proof of Residency: Documents like utility bills, driver’s license, or voter registration can help establish the home as your principal residence.

- Income Verification: W-2s, 1099s, and other income statements will be necessary to confirm you meet any income limitations.

- Proof of First-Time Homebuyer Status: While often self-certified, having records demonstrating you haven’t owned a principal residence in the last two years can be helpful.

Keeping these documents organized in a dedicated file will make the tax filing process much smoother and ensure you have everything ready if the IRS requires further verification for your homebuyer tax credits claim.

Filing Your Tax Return

The 2026 homebuyer tax credits will be claimed when you file your federal income tax return for the tax year 2026 (which you typically do in early 2027). The IRS will provide a specific form or schedule that you will need to complete and attach to your Form 1040. This form will require you to enter details about your home purchase, confirm your eligibility, and calculate the amount of your credit.

It’s highly recommended to use tax software or consult with a qualified tax professional to ensure accurate filing. Tax laws can be complex, and a professional can help you navigate the specific requirements for the homebuyer tax credits, ensuring you claim the maximum amount you’re entitled to while avoiding common errors. They can also advise on how these federal credits interact with any state or local homebuyer programs you might be utilizing.

Potential for Advance Payments or Rebates

While most tax credits are claimed when filing your annual return, there has been discussion in some proposals for the possibility of an advance payment or rebate for the homebuyer tax credits. This would mean that eligible homebuyers could receive a portion of the credit at the time of closing, rather than waiting until tax season. If this provision is included in the final legislation, it would provide immediate financial relief, which could be incredibly beneficial for covering upfront costs. However, advance payments often come with additional administrative requirements and safeguards to prevent fraud.

Stay tuned for updates on this specific aspect of the new homebuyer tax credits. If an advance payment option becomes available, it would significantly alter the claiming process and offer a more direct benefit at the point of purchase. Regardless, proper documentation and understanding of the rules will be paramount.

Maximizing Your $8,000 Federal Incentives

An $8,000 tax credit is a substantial benefit, and understanding how to maximize its impact can make a significant difference in your homeownership journey. This isn’t just about claiming the credit; it’s about integrating it into your overall financial planning for your new home. Strategic planning can ensure you get the most out of these valuable homebuyer tax credits.

Combining Federal, State, and Local Programs

The 2026 federal homebuyer tax credits are often just one piece of a larger puzzle of homeownership assistance. Many states and local municipalities offer their own programs, which can include down payment assistance, closing cost grants, or additional tax credits. Researching and combining these programs can lead to even greater savings.

- State Housing Finance Agencies (HFAs): Most states have HFAs that offer various loan programs and assistance specifically for first-time homebuyers. These often come with competitive interest rates and down payment assistance.

- Local Municipality Programs: Cities and counties may have programs funded by local bonds or grants, targeting specific areas or demographics.

- Employer-Assisted Housing: Some employers offer benefits to help employees purchase homes, especially in high-cost areas.

When looking into these options, always verify if they can be stacked with federal homebuyer tax credits. In many cases, they can, providing a truly comprehensive financial aid package for your home purchase.

Financial Planning and Budgeting for Homeownership

While the homebuyer tax credits provide a welcome financial boost, they are not a substitute for sound financial planning. Homeownership comes with ongoing costs beyond the mortgage, including property taxes, insurance, maintenance, and utilities. Incorporating the expected tax credit into your budget can help, but a realistic assessment of all expenses is vital.

- Down Payment Strategy: Use the credit to supplement your down payment savings, potentially allowing you to reach the 20% threshold and avoid private mortgage insurance (PMI).

- Closing Costs: These can often be 2-5% of the loan amount. The credit can significantly offset these upfront expenses.

- Emergency Fund: Always maintain an emergency fund for unexpected home repairs or job loss. The credit can free up other funds to bolster this reserve.

- Long-Term Financial Goals: Consider how homeownership fits into your broader financial goals, such as retirement planning or college savings.

A well-thought-out financial plan, integrating the homebuyer tax credits, will set you up for long-term success as a homeowner.

Consulting with Experts

The journey to homeownership, especially when leveraging government incentives like the 2026 homebuyer tax credits, is best undertaken with professional guidance. Engaging with experts can ensure you understand all the intricacies and make informed decisions.

- Tax Professional: A Certified Public Accountant (CPA) or an enrolled agent can provide invaluable advice on eligibility, documentation, and proper filing of your tax return to claim the credit. They can also help you understand any recapture provisions.

- Mortgage Lender: An experienced mortgage lender can guide you through loan options, explain how the tax credit might impact your affordability, and ensure your loan aligns with any program requirements.

- Real Estate Agent: A knowledgeable real estate agent can help you find homes that meet the purchase price limits and other criteria associated with the homebuyer tax credits.

- Housing Counselors: HUD-approved housing counseling agencies offer free or low-cost advice on home buying, rental, and foreclosure prevention.

These professionals can help you navigate the complexities of the housing market and tax code, ensuring you maximize the benefits of the new homebuyer tax credits and make the best financial decisions for your future.

Common Questions and Misconceptions About Homebuyer Tax Credits

Even with clear guidelines, tax credits can often lead to questions and misunderstandings. Addressing these common queries about the 2026 homebuyer tax credits can help you approach your home purchase with confidence and clarity.

Is This Only for First-Time Homebuyers?

While the primary focus of many federal homebuyer incentives, including the anticipated 2026 homebuyer tax credits, is indeed on first-time homebuyers, it’s not always exclusively so. As discussed earlier, the definition of a ‘first-time homebuyer’ typically includes anyone who hasn’t owned a principal residence in the past two to three years. This means that individuals who previously owned a home but have been out of the market for a qualifying period may still be eligible.

Furthermore, some past credits have included provisions for specific groups, such as those purchasing homes in economically distressed areas or certain public service professionals. It’s crucial to review the final legislation for the 2026 homebuyer tax credits to understand if any exceptions or broader eligibility criteria apply beyond the standard first-time homebuyer definition. Never assume you’re ineligible without thoroughly checking the official guidelines.

Do I Have to Pay Back the Credit?

This is a critical question, and the answer depends on the specific design of the 2026 homebuyer tax credits. Historically, some federal homebuyer tax credits have included a ‘recapture’ provision. This means that if you sold the home within a certain period (e.g., 36 months) after claiming the credit, you might have to repay a portion or all of the credit back to the IRS. The intent of such provisions is to encourage sustained homeownership and prevent people from using the credit for short-term gains.

It is absolutely essential to understand whether the 2026 homebuyer tax credits will include a recapture clause. If it does, you’ll need to factor this into your long-term plans. If you anticipate needing to sell the home within a few years of purchase, the implications of a recapture provision could significantly affect your financial calculations. Always consult with a tax advisor to fully understand the terms and conditions related to repayment, if applicable.

How Does the Credit Impact My Mortgage?

The 2026 homebuyer tax credits primarily impact your tax liability, not directly your mortgage loan itself. However, there are indirect ways it can influence your mortgage and overall home financing:

- Down Payment: By freeing up funds (either by reducing your tax bill or through an advance payment), the credit can effectively increase your available capital for a down payment. A larger down payment can lead to a smaller loan amount, lower monthly payments, and potentially better interest rates.

- Closing Costs: These can often be 2-5% of the loan amount. The credit can significantly offset these upfront expenses.

- Affordability: By reducing your overall financial burden, the credit can make homeownership more affordable, potentially allowing you to qualify for a loan you might not have otherwise afforded, or to purchase a slightly more expensive home within your budget.

- Debt-to-Income Ratio: While the credit itself doesn’t directly alter your debt-to-income (DTI) ratio, the financial flexibility it provides can indirectly help manage your overall financial picture, which lenders review.

It’s important to remember that the credit is generally treated as a reimbursement or reduction in taxes, not an upfront cash gift directly from the mortgage lender. Discuss with your lender how they factor in anticipated tax credits when assessing your loan eligibility and affordability.

Preparing for Homeownership in 2026

The announcement of new homebuyer tax credits for 2026 provides a fantastic opportunity, but successful homeownership requires more than just a tax break. Proactive preparation can make your home-buying journey smoother and more rewarding. Leveraging these homebuyer tax credits effectively means being ready for the market.

Improving Your Credit Score

Your credit score is a critical factor in securing a mortgage and getting favorable interest rates. Lenders use your score to assess your creditworthiness. A higher credit score can translate to thousands of dollars in savings over the life of your loan. Start working on improving your score well in advance of your home purchase:

- Check Your Credit Report: Obtain free copies of your credit report from Equifax, Experian, and TransUnion. Dispute any errors.

- Pay Bills on Time: Payment history is the most significant factor in your credit score.

- Reduce Debt: Lowering your credit utilization ratio (the amount of credit you’re using compared to your total available credit) can boost your score.

- Avoid New Credit: Refrain from opening new credit accounts or making large purchases on credit before applying for a mortgage.

A strong credit score will not only help you qualify for a mortgage but also ensure you get the best possible terms, maximizing the impact of the homebuyer tax credits.

Saving for a Down Payment and Closing Costs

Even with the potential $8,000 from the homebuyer tax credits, saving for a down payment and closing costs remains crucial. While a 20% down payment is ideal to avoid PMI, many loan programs allow for much lower down payments (e.g., 3-5%). However, the more you put down, the less you borrow, and the lower your monthly payments will be.

- Create a Savings Plan: Set a realistic savings goal and timeline.

- Automate Savings: Set up automatic transfers from your checking to a dedicated savings account.

- Cut Unnecessary Expenses: Temporarily reduce discretionary spending to accelerate your savings.

- Explore Gift Funds: Inquire if family members are willing to provide gift funds, which are often allowed under specific conditions for down payments.

The homebuyer tax credits can certainly alleviate some of this burden, but a solid savings foundation will put you in a much stronger financial position.

Getting Pre-Approved for a Mortgage

Before you even start seriously looking at homes, getting pre-approved for a mortgage is a vital step. A pre-approval letter from a lender indicates that you have been conditionally approved for a loan up to a certain amount. This offers several benefits:

- Know Your Budget: You’ll have a clear understanding of how much home you can afford, preventing you from looking at properties outside your price range.

- Show Serious Intent: Sellers and their agents will take your offer more seriously if you’re pre-approved, giving you an edge in competitive markets.

- Streamline the Process: It speeds up the closing process once you find a home, as much of the financial vetting has already been done.

- Identify Issues Early: Any potential issues with your credit or financial history can be identified and addressed before you’re under contract.

Discuss the upcoming homebuyer tax credits with your lender during the pre-approval process. While they may not be able to factor it into your immediate loan qualification, they can advise on how it will impact your overall financial picture post-closing.

The Future of Homeownership and Federal Support

The introduction of new homebuyer tax credits for 2026 underscores a continuing commitment from the federal government to support homeownership. These incentives are more than just financial breaks; they represent an investment in individual wealth building, community stability, and economic growth.

Long-Term Impact of Homebuyer Tax Credits

Federal incentives like the 2026 homebuyer tax credits have a ripple effect. They not only assist individual buyers but also:

- Stimulate the Housing Market: By increasing demand, they can boost construction, real estate transactions, and related industries.

- Promote Economic Stability: A healthy housing market is often a strong indicator of overall economic well-being.

- Encourage Savings: Knowing a credit is available can motivate potential buyers to save more for a down payment.

- Reduce Wealth Inequality: Homeownership is a primary driver of wealth accumulation for many families, and these credits help make it accessible to a broader demographic.

Understanding these broader impacts helps contextualize the importance of the homebuyer tax credits and why such programs are periodically enacted.

Staying Informed for Future Opportunities

The landscape of federal housing assistance can change. While the 2026 homebuyer tax credits are a current focus, it’s wise to remain informed about future legislative changes and potential new programs. Subscribe to government updates, follow reputable financial news outlets, and maintain a relationship with a trusted tax advisor and mortgage professional. This proactive approach ensures you’re always aware of opportunities to make homeownership more affordable and sustainable.

The dream of owning a home is within reach for many, and the new homebuyer tax credits for 2026 offer a powerful tool to turn that dream into a reality. By understanding the eligibility criteria, preparing your finances, and leveraging expert advice, you can confidently navigate the path to homeownership and claim the substantial federal incentives available to you.

")