2026 Social Security COLA: Navigating the 3.2% Adjustment and Retiree Budgets

The 2026 Social Security COLA: Understanding the 3.2% Adjustment and Its Impact on Retiree Budgets

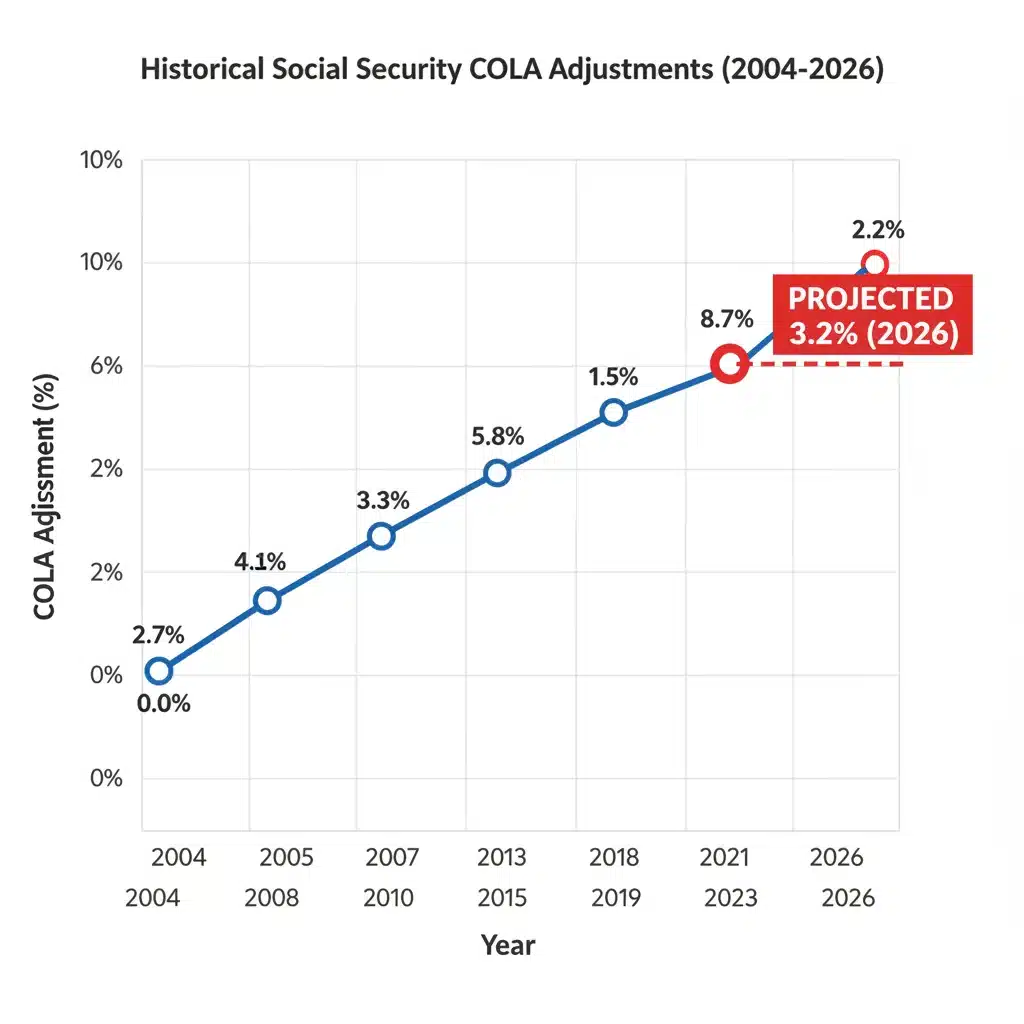

As millions of Americans approach or enter retirement, one of the most critical factors influencing their financial well-being is the annual Social Security Cost-of-Living Adjustment, or COLA. This adjustment is designed to help Social Security beneficiaries keep pace with inflation and maintain their purchasing power. For 2026, projections are beginning to solidify, with a notable Social Security COLA 2026 of approximately 3.2% on the horizon. This figure, while still a projection, carries significant implications for the financial strategies and daily lives of retirees across the nation.

Understanding the intricacies of the COLA, how it’s calculated, and its potential impact on your personal finances is paramount. This comprehensive guide will delve deep into the anticipated 3.2% adjustment for 2026, explore the methodology behind its determination, analyze its effects on retiree budgets, and offer strategic advice for navigating these changes effectively. Whether you are currently receiving Social Security benefits, planning for future retirement, or simply interested in the economic factors that shape senior finances, this article provides essential insights into the Social Security COLA 2026.

What is the Social Security COLA and Why is it Important?

The Cost-of-Living Adjustment (COLA) is an annual increase in Social Security and Supplemental Security Income (SSI) benefits. Its primary purpose, as mandated by law, is to ensure that the purchasing power of Social Security benefits is not eroded by inflation. Without COLA, the fixed income of retirees would steadily lose value over time as the cost of goods and services rises, leading to a decline in their standard of living. This mechanism is a cornerstone of financial stability for millions of older Americans and other beneficiaries.

The importance of COLA cannot be overstated. For many retirees, Social Security benefits represent a significant, if not primary, source of their income. A meaningful adjustment can mean the difference between comfortably covering essential expenses and struggling to make ends meet. Conversely, a low or non-existent COLA, as seen in some years, can present considerable financial challenges, especially during periods of high inflation. The Social Security COLA 2026, projected at 3.2%, aims to offer a substantial boost to beneficiaries, reflecting continued inflationary pressures.

The calculation of the COLA is tied to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Specifically, the Social Security Administration (SSA) compares the average CPI-W for the third quarter (July, August, and September) of the current year with the average CPI-W for the same period of the last year in which a COLA was enacted. The percentage increase between these two periods determines the COLA for the upcoming year. If there is no increase, there is no COLA. This direct link to a specific inflation measure ensures that the adjustment is data-driven and responsive to economic realities faced by a significant segment of the population.

While the CPI-W is designed to reflect the spending habits of urban wage earners, critics often argue that it may not fully capture the unique expenditure patterns of retirees, who typically spend more on healthcare and housing and less on transportation or certain consumer goods. This debate is ongoing, but for now, the CPI-W remains the official metric for determining the Social Security COLA 2026 and all subsequent adjustments.

The 2026 Social Security COLA Projection: 3.2% Explained

The projection of a 3.2% Social Security COLA 2026 is based on current economic forecasts and inflation trends. While the official announcement typically occurs in October of the preceding year (in this case, October 2025), economists and financial analysts use available CPI-W data and other economic indicators to provide early estimates. These projections are crucial for retirees and financial planners to anticipate future income levels and adjust their budgets accordingly.

A 3.2% increase, if realized, would translate into a tangible rise in monthly benefits for millions. For instance, if the average monthly Social Security benefit for retired workers is currently around $1,900, a 3.2% COLA would add approximately $60.80 to their monthly payment. While this might seem modest to some, for individuals relying heavily on Social Security, such an increase can significantly impact their ability to cover rising costs for necessities like food, utilities, and healthcare.

Several factors contribute to the projected 3.2% COLA for 2026. Persistent inflation, although showing signs of moderation, continues to be a driving force. Supply chain issues, geopolitical events, and labor market dynamics all play a role in shaping consumer prices. The Federal Reserve’s monetary policy, aimed at curbing inflation, also indirectly influences the COLA by affecting the overall economic environment. Analysts monitor these interwoven factors closely to refine their COLA predictions.

It’s important to remember that these are projections. The final COLA could be slightly higher or lower depending on how the CPI-W performs during the third quarter of 2025. Unexpected economic shifts, such as a sudden surge or decline in energy prices, could alter the outcome. However, a 3.2% projection provides a strong indication of what beneficiaries can realistically expect for their Social Security COLA 2026.

This projected increase follows a period of historically high COLA adjustments in recent years, a direct response to elevated inflation. While 3.2% is lower than the adjustments seen in 2022 and 2023, it still represents a solid increase that demonstrates the ongoing need to protect retiree purchasing power against the backdrop of a dynamic economic landscape. The consistency of these adjustments underscores the vital role Social Security plays in providing a financial safety net.

Impact on Retiree Budgets: Navigating the 3.2% Increase

A 3.2% Social Security COLA 2026 will undoubtedly have a noticeable impact on retiree budgets, influencing everything from daily spending to long-term financial planning. For some, it will provide much-needed relief from the relentless march of inflation, allowing them to maintain their current lifestyle without significant cutbacks. For others, particularly those with higher expenses or limited supplementary income, it might still feel like a modest adjustment in the face of ever-increasing costs.

Healthcare Costs: A Persistent Challenge

One of the most significant expenditures for retirees is healthcare. While Social Security benefits increase, so too do Medicare premiums, deductibles, and out-of-pocket expenses. Medicare Part B premiums, for example, are typically deducted directly from Social Security checks. If the increase in Part B premiums outpaces the COLA, the net benefit increase for some individuals might be less than anticipated, or even result in a slight decrease in discretionary income. This phenomenon, sometimes referred to as the "hold harmless" provision, ensures that most beneficiaries’ net Social Security payment doesn’t decrease due to rising Part B premiums, but it doesn’t prevent the COLA from being largely consumed by these costs.

Therefore, when considering the 3.2% Social Security COLA 2026, it’s crucial for retirees to also factor in expected increases in healthcare costs. Proactive planning, including reviewing Medicare plan options and exploring supplemental insurance, can help mitigate these financial pressures. Even with a COLA, healthcare remains a dominant financial concern for the elderly.

Rising Cost of Goods and Services

Beyond healthcare, retirees face rising costs for everyday essentials: groceries, utilities, housing, and transportation. A 3.2% COLA aims to offset these increases. However, individual spending patterns vary greatly. A retiree who drives frequently might feel a greater pinch from high gas prices, while another living in an area with rapidly escalating property taxes or rents might find housing costs to be the primary budget strain. The CPI-W, while broad, may not perfectly align with every individual’s specific inflation experience.

The Social Security COLA 2026 is a blanket adjustment; it doesn’t distinguish between different geographic regions or spending habits. Thus, while it provides a general uplift, retirees in high-cost-of-living areas might find the 3.2% increase less impactful than those in more affordable regions. This highlights the importance of personalized budgeting and financial assessment.

Tax Implications

Another aspect often overlooked is the potential tax implications of a COLA. For some beneficiaries, an increase in Social Security benefits can push their combined income (adjusted gross income plus half of Social Security benefits) above certain thresholds, making a portion of their Social Security benefits taxable. This means that while their gross benefit increases by 3.2%, their net, after-tax income might not rise by the full percentage, or could even be subject to new tax liabilities.

Understanding these thresholds and consulting with a tax advisor can help retirees plan for the tax consequences of the Social Security COLA 2026. Proactive tax planning is an integral part of maximizing the benefit of any COLA adjustment, ensuring that the intended increase in purchasing power is not inadvertently diminished by higher tax obligations. This complex interplay between benefits and taxes requires careful consideration.

Strategies for Maximizing Your Social Security Benefits and Financial Well-being

Given the projected 3.2% Social Security COLA 2026 and the ongoing economic landscape, retirees and pre-retirees can adopt several strategies to optimize their financial situation and ensure their Social Security benefits go further.

1. Re-evaluate Your Budget Annually

With each COLA announcement, it’s an opportune time to revisit and revise your household budget. Update your income figures to reflect the new Social Security benefit amount. More importantly, review your expenses. Are there areas where you can cut back? Are your utility costs rising faster than anticipated? Are you spending more on groceries than planned? A thorough annual budget review helps you understand where your money is going and how the COLA impacts your overall financial health.

Consider using budgeting tools or spreadsheets to track your income and expenses. This granular approach allows you to identify trends and make informed decisions. The 3.2% Social Security COLA 2026, while helpful, should be integrated into a realistic and regularly updated financial plan. Don’t assume the COLA will perfectly cover all rising costs; actively manage your spending.

2. Optimize Healthcare Spending

Healthcare is a dynamic and often costly component of retirement. Each year during the Medicare Open Enrollment Period, review your Medicare Advantage (Part C) or Prescription Drug (Part D) plans. Premiums, deductibles, and formularies can change, and a plan that was ideal one year might not be the best fit the next. Comparing plans can lead to significant savings, effectively stretching the impact of your Social Security COLA 2026.

Additionally, explore options like Medicare Supplement (Medigap) plans to cover gaps in original Medicare, or investigate state-specific assistance programs for low-income seniors. Being an informed consumer of healthcare services can protect your budget from unexpected medical expenses and make your COLA more impactful.

3. Consider Part-Time Work or "Encore Career"

For many retirees, a 3.2% COLA, while welcome, might not be enough to comfortably cover all expenses, especially if they have limited savings or other income sources. Engaging in part-time work, volunteering that offers stipends, or pursuing an "encore career" can supplement Social Security benefits. This not only boosts income but can also provide social engagement and a sense of purpose. It’s important to understand the Social Security earnings test if you are under full retirement age, as earning too much can temporarily reduce your benefits.

Even a few hours of work per week can make a substantial difference, particularly when combined with the Social Security COLA 2026. This additional income can be used to cover discretionary spending, build an emergency fund, or simply provide a greater sense of financial security.

4. Review Investment Portfolios

If you have retirement savings in 401(k)s, IRAs, or other investment accounts, regularly review your portfolio with a financial advisor. Ensure your asset allocation aligns with your risk tolerance and withdrawal strategy. A well-managed portfolio can provide supplementary income that complements your Social Security benefits, helping to offset any shortfalls even with the Social Security COLA 2026.

Consider strategies like systematic withdrawals or dividend-paying investments to create a consistent stream of income. A diversified portfolio can help protect against market volatility while generating growth that supports your retirement lifestyle. Don’t let your investments stagnate; active management is key to long-term financial health.

5. Understand Your Full Retirement Age and Claiming Strategy

For those not yet claiming Social Security, understanding your Full Retirement Age (FRA) and various claiming strategies is paramount. While this article focuses on the Social Security COLA 2026, the decision of when to claim benefits has a much larger and permanent impact on your monthly payout. Delaying benefits beyond your FRA, up to age 70, can result in significantly higher monthly payments due to delayed retirement credits. These credits can increase your benefit by 8% per year.

Conversely, claiming early (as early as age 62) will result in a permanently reduced benefit. The COLA applies to whatever benefit amount you are receiving, so a higher starting benefit due to delayed claiming will result in a larger dollar increase from any future COLA, including the Social Security COLA 2026. This is a complex decision that should be made after careful consideration of your health, other income sources, and life expectancy, often with the guidance of a financial advisor.

6. Be Mindful of "Windfall Elimination Provision" and "Government Pension Offset"

Some retirees, particularly those who worked in jobs not covered by Social Security (e.g., certain government employees, teachers in some states) but also worked in Social Security-covered employment, might be affected by the Windfall Elimination Provision (WEP) or the Government Pension Offset (GPO). These provisions can significantly reduce Social Security benefits for individuals receiving a pension from non-covered employment. It’s critical for those potentially affected to understand how these rules interact with their Social Security benefits and any COLA, including the Social Security COLA 2026, as they can impact the actual increase received.

These provisions are often misunderstood and can lead to unexpected reductions. If you have worked in both covered and non-covered employment, it is highly advisable to contact the Social Security Administration or a financial planner specializing in Social Security to understand how WEP or GPO might affect your benefits and the real impact of any COLA.

The Broader Economic Context: Inflation and the Future of Social Security

The projected 3.2% Social Security COLA 2026 does not exist in a vacuum; it is a direct reflection of broader economic trends, particularly inflation. While inflation has cooled from its recent peaks, it remains elevated compared to pre-pandemic levels. This persistent inflation impacts not only retirees but also the broader economy, influencing everything from interest rates to consumer confidence.

The Federal Reserve’s ongoing efforts to bring inflation down to its 2% target will continue to shape the economic environment. Successful inflation control could lead to more stable, albeit potentially lower, COLA adjustments in the future. Conversely, a resurgence of inflationary pressures could result in higher COLA figures, but also greater economic uncertainty for all.

Beyond inflation, the long-term solvency of Social Security is a perennial topic of discussion. While the COLA addresses short-term purchasing power, the system’s ability to pay full benefits in the distant future depends on demographic trends, economic growth, and legislative actions. The Social Security trust funds are projected to be able to pay 100% of scheduled benefits until the mid-2030s, after which they would be able to pay about 80% if no legislative changes are made. This long-term outlook is a separate, but related, concern for beneficiaries.

The Social Security COLA 2026 is a vital component of the system, ensuring current beneficiaries can meet their daily needs. However, a holistic view of retirement planning must also encompass the broader economic context and the future of Social Security itself. Staying informed about legislative proposals and economic forecasts is crucial for making sound long-term financial decisions.

Conclusion: Preparing for the 2026 Social Security COLA

The anticipated 3.2% Social Security COLA 2026 offers a significant, albeit modest, adjustment for millions of beneficiaries. While it aims to protect against inflation, the real impact on individual budgets will vary depending on personal circumstances, spending habits, and other income sources. Proactive financial planning, including regular budget reviews, optimized healthcare spending, and strategic investment management, remains essential for navigating the complexities of retirement finances.

Understanding how the COLA is calculated, its potential effects on taxes and Medicare premiums, and the broader economic forces at play empowers retirees to make informed decisions. As the official announcement for the 2026 COLA approaches in October 2025, staying updated with economic news and consulting with financial professionals will be key. The Social Security COLA 2026 is more than just a percentage; it’s a critical lifeline that helps ensure a more secure and stable retirement for those who rely on it.

By taking a comprehensive approach to financial planning, retirees can effectively leverage the Social Security COLA 2026 to their advantage, maintaining their purchasing power and enjoying a well-deserved retirement.