Roth IRA Limits 2026: Maximize Your Tax-Free Retirement Savings

In the ever-evolving landscape of personal finance, planning for retirement requires foresight, adaptability, and a keen understanding of the rules governing tax-advantaged accounts. Among the most popular and powerful tools for retirement savings is the Roth IRA, renowned for its tax-free withdrawals in retirement. As we look towards 2026, understanding the projected Roth IRA Limits 2026 and income thresholds becomes paramount for anyone aiming to maximize their long-term wealth accumulation.

The Roth IRA offers a unique advantage: contributions are made with after-tax dollars, meaning qualified withdrawals in retirement are completely tax-free. This benefit makes it an incredibly attractive option, especially for younger individuals who anticipate being in a higher tax bracket during retirement than they are today, or for those who simply appreciate the certainty of tax-free income in their golden years. However, this powerful tool comes with certain restrictions, specifically regarding income levels and contribution amounts, which are adjusted annually for inflation.

While the official figures for 2026 are not yet released by the IRS, we can make informed projections based on historical trends and current economic indicators. This comprehensive guide will delve into what you need to know about the anticipated Roth IRA Limits 2026, including contribution limits, income phase-out ranges, and strategies to navigate these rules effectively. Whether you’re a seasoned investor or just starting your retirement savings journey, staying informed about these changes is crucial for optimizing your financial strategy.

Understanding the Roth IRA: A Quick Refresher

Before we dive into the specifics of the Roth IRA Limits 2026, let’s briefly revisit the core principles of a Roth IRA. Established as part of the Taxpayer Relief Act of 1997, the Roth IRA has grown to become a cornerstone of many Americans’ retirement plans. Unlike a Traditional IRA, where contributions may be tax-deductible and withdrawals are taxed in retirement, Roth IRA contributions are made with after-tax money. The magic happens at withdrawal: if certain conditions are met, all qualified distributions – including both contributions and earnings – are entirely tax-free.

This tax-free growth and withdrawal feature is particularly appealing for several reasons:

- Tax Diversification: A Roth IRA provides tax diversification in retirement. By having both pre-tax (like a 401(k) or Traditional IRA) and post-tax (Roth IRA) accounts, you have more flexibility to manage your tax burden in retirement, depending on future tax rates.

- No Required Minimum Distributions (RMDs) for the Original Owner: Unlike Traditional IRAs, Roth IRAs do not have RMDs for the original owner during their lifetime. This allows your money to continue growing tax-free for as long as you live, and you can pass it on to your beneficiaries.

- Flexibility with Contributions: While the primary purpose is retirement, you can withdraw your contributions (not earnings) from a Roth IRA at any time, tax-free and penalty-free, for any reason. This offers a degree of liquidity that other retirement accounts often lack.

- Estate Planning Benefits: The ability to pass on a Roth IRA to beneficiaries, who can then take tax-free withdrawals, makes it an excellent estate planning tool.

However, accessing these benefits is contingent on meeting specific eligibility criteria, most notably related to your Modified Adjusted Gross Income (MAGI) and annual contribution limits. These are the very limits we’ll explore for the upcoming year.

Projected Roth IRA Contribution Limits 2026

The Internal Revenue Service (IRS) typically announces the official contribution limits for IRAs and 401(k)s in the late fall of the preceding year. While we don’t have the definitive numbers for 2026 yet, we can make educated guesses based on inflation trends. The contribution limits are adjusted in $500 increments, and given recent inflationary pressures, it’s highly probable we’ll see an increase.

For context, the Roth IRA contribution limit for 2024 is $7,000 for those under age 50, and $8,000 for those age 50 and over (including the $1,000 catch-up contribution). Based on historical adjustments and current economic projections, we anticipate the Roth IRA contribution limits for 2026 to be:

- Under Age 50: Potentially $7,500 or $8,000

- Age 50 and Over: Potentially $8,500 or $9,000 (including the catch-up contribution)

These are projections, and the actual numbers may vary. It’s crucial to consult official IRS announcements when they become available. Regardless of the exact figure, the principle remains: consistently contributing the maximum allowed amount each year is one of the most effective strategies for maximizing your tax-free retirement nest egg. Even small increases in the contribution limit can lead to substantial growth over decades due to the power of compound interest.

It’s important to remember that these limits apply to your total contributions across all your IRAs (Traditional and Roth combined). You cannot contribute the maximum to both a Traditional and a Roth IRA in the same year; the combined total cannot exceed the annual limit.

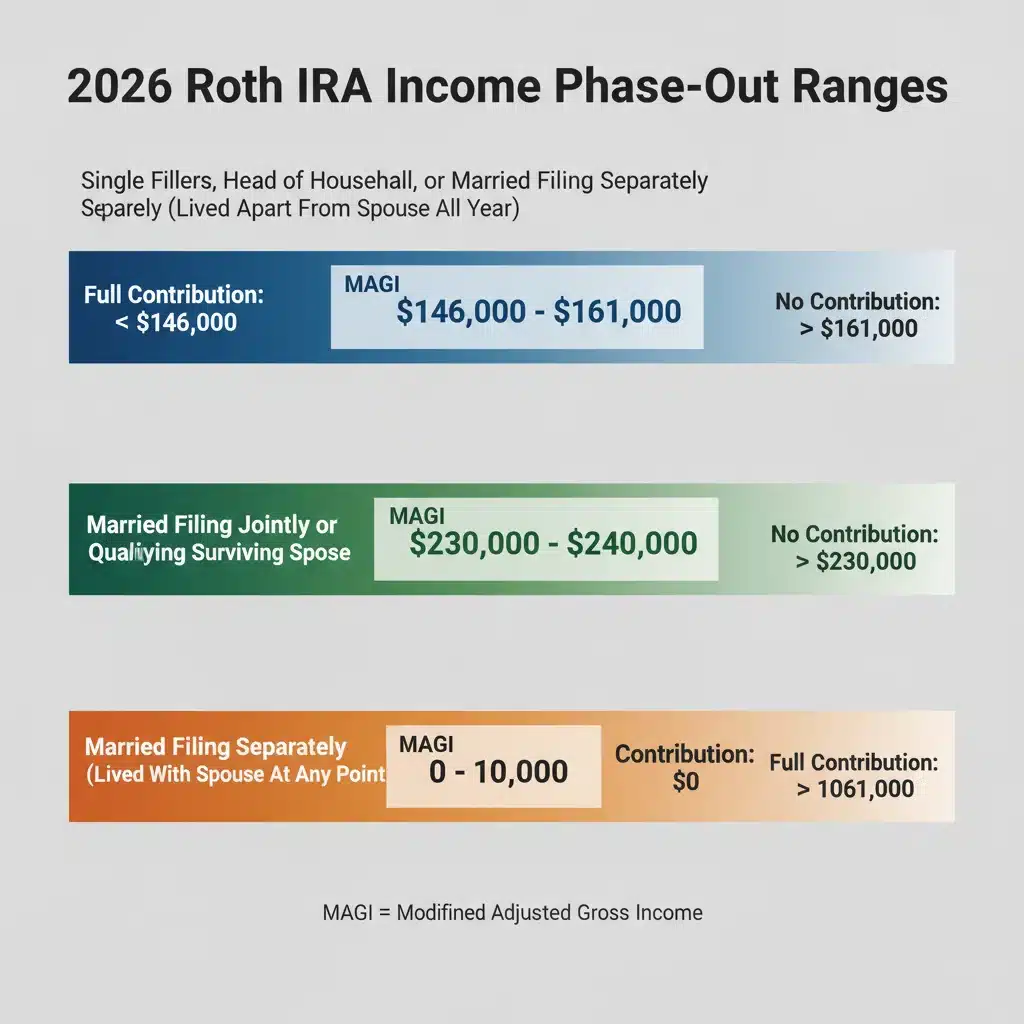

Roth IRA Income Limits 2026: Projected Phase-Out Ranges

The most significant hurdle for many high-income earners when it comes to Roth IRAs is the income limitation. The ability to contribute directly to a Roth IRA phases out once your Modified Adjusted Gross Income (MAGI) reaches certain thresholds. These thresholds are also adjusted annually for inflation.

For 2024, the MAGI phase-out ranges are:

- Single Filers, Heads of Household, and Married Filing Separately (if you did not live with your spouse at any time during the year): Contributions begin to phase out at $146,000 and are completely phased out at $161,000.

- Married Filing Jointly and Qualifying Widow(er): Contributions begin to phase out at $230,000 and are completely phased out at $240,000.

Given the inflationary environment, we can anticipate these income thresholds to increase for 2026. While precise figures are speculative, based on historical adjustments, we might see the Roth IRA income limits 2026 for MAGI phase-out ranges as follows:

- Single Filers, Heads of Household, and Married Filing Separately: Phase-out might begin around $150,000 – $155,000 and be completely phased out around $165,000 – $170,000.

- Married Filing Jointly and Qualifying Widow(er): Phase-out might begin around $235,000 – $245,000 and be completely phased out around $245,000 – $255,000.

It’s vital to understand your MAGI, as it determines your eligibility to contribute directly to a Roth IRA. Your MAGI is your adjusted gross income (AGI) with certain deductions added back. Common deductions that are added back include deductions for IRA contributions, student loan interest, and tuition and fees. Always consult a tax professional or reliable tax software to calculate your precise MAGI.

If your income falls within the phase-out range, you can only contribute a reduced amount. If your income exceeds the upper limit of the phase-out range, you are not permitted to make direct contributions to a Roth IRA for that year.

Even if you find your income approaching or exceeding the Roth IRA income limits 2026, there are still several strategies you can employ to benefit from the tax advantages of a Roth account:

The Backdoor Roth IRA Strategy

For high-income earners who are phased out of direct Roth IRA contributions, the "backdoor Roth IRA" strategy is an invaluable tool. This involves making a non-deductible contribution to a Traditional IRA and then immediately converting that Traditional IRA into a Roth IRA. Since the initial contribution was non-deductible, there’s typically no tax due on the conversion (assuming you have no other pre-tax IRA money). This strategy effectively bypasses the income limitations for direct Roth contributions.

Steps for a Backdoor Roth IRA:

- Contribute to a Non-Deductible Traditional IRA: Contribute the maximum allowed amount to a Traditional IRA. Ensure you designate this contribution as non-deductible on IRS Form 8606.

- Convert to a Roth IRA: Shortly after, convert the Traditional IRA balance to a Roth IRA.

- File Form 8606: When you file your taxes, you’ll need to report both the non-deductible contribution and the conversion on Form 8606, "Nondeductible IRAs."

Important Considerations for Backdoor Roth:

- Pro-Rata Rule: The "pro-rata rule" is crucial. If you have any existing pre-tax money in other Traditional IRAs (including SEP IRAs or SIMPLE IRAs), a portion of your conversion will be taxable. The IRS views all your Traditional IRA accounts as one for tax purposes. If you have, for example, $90,000 in a pre-tax Traditional IRA and you contribute $10,000 non-deductible, then convert the $10,000, 90% of that conversion ($9,000) would be taxable. To avoid this, it’s often advisable to roll any existing pre-tax IRA money into a 401(k) or similar employer-sponsored plan before performing a backdoor Roth.

- Timing: While there’s no strict rule, converting immediately after contribution minimizes potential earnings on the non-deductible contribution, which would otherwise be taxable upon conversion.

The backdoor Roth IRA remains a legitimate and widely used strategy. However, tax laws can change, so it’s always wise to stay updated on any legislative developments that could impact this strategy.

Employer-Sponsored Roth Options: Roth 401(k) and Roth 403(b)

Another excellent way to contribute after-tax money for tax-free growth is through employer-sponsored Roth accounts, such as a Roth 401(k) or Roth 403(b). These accounts have much higher contribution limits than Roth IRAs and, crucially, do not have income limitations for contributions. This means even high-income earners can contribute directly to a Roth 401(k).

For 2024, the 401(k) contribution limit is $23,000, with an additional $7,500 catch-up contribution for those age 50 and over. While 2026 limits are not yet available, we can expect them to be higher, potentially reaching $24,000 – $25,000 for regular contributions and $8,000 – $8,500 for catch-up contributions.

If your employer offers a Roth 401(k), it’s an excellent option to consider, especially if you exceed the Roth IRA income limits 2026. The tax advantages are similar to a Roth IRA: after-tax contributions and tax-free withdrawals in retirement, provided certain conditions are met.

Mega Backdoor Roth (if available)

For those with a 401(k) plan that permits after-tax contributions (beyond the regular pre-tax or Roth 401(k) limits) and in-service distributions or rollovers, the "mega backdoor Roth" could be an option. This strategy involves:

- Contributing the maximum to your traditional or Roth 401(k).

- Contributing additional after-tax dollars to your 401(k) (up to the overall 401(k) limit, which is much higher, at $69,000 for 2024).

- Converting these after-tax 401(k) contributions into a Roth IRA or Roth 401(k).

This strategy allows for significant amounts of money to be moved into a Roth account, far exceeding the standard Roth IRA Limits 2026. However, it requires a specific 401(k) plan design, so check with your plan administrator if this is an option for you.

The Impact of Inflation on Roth IRA Limits

The annual adjustments to Roth IRA contribution limits and income phase-out ranges are primarily driven by inflation. The IRS uses specific inflation metrics to determine these changes, ensuring that the purchasing power of your retirement savings is preserved over time. In periods of higher inflation, we tend to see more significant increases in these limits.

Understanding this mechanism is important for long-term planning. While we project the Roth IRA Limits 2026, it’s the underlying economic conditions that dictate the actual figures. Persistent inflation means that the dollar amounts you can contribute and the income thresholds for eligibility will likely continue to rise, albeit in increments.

This also underscores the importance of reviewing your retirement strategy annually. What was true for 2024 or 2025 might shift for 2026, and staying updated allows you to make timely adjustments to your contributions and financial planning.

Why the Roth IRA is a Powerful Retirement Vehicle

Beyond the specific Roth IRA Limits 2026, it’s worth reiterating why this account type remains a cornerstone of effective retirement planning for so many. Its unique benefits offer distinct advantages that can significantly impact your financial well-being in retirement.

Tax-Free Growth and Withdrawals

This is the primary allure. Imagine contributing to an account for 30 or 40 years, watching it grow significantly, and then being able to withdraw every dollar – contributions and earnings – completely tax-free. This is particularly valuable if you expect to be in a higher tax bracket in retirement, perhaps due to other income sources or rising tax rates in the future. The certainty of tax-free income provides peace of mind and simplifies retirement budgeting.

Flexibility and Accessibility

As mentioned, you can withdraw your contributions from a Roth IRA at any time, tax-free and penalty-free. While not advisable for regular spending, this feature provides an emergency fund or a safety net that traditional retirement accounts typically don’t offer. This flexibility can be a significant advantage, especially for younger savers who might face unexpected financial needs before retirement.

No RMDs for Original Owner

The absence of Required Minimum Distributions (RMDs) during your lifetime is a major benefit. This means your money can continue to grow tax-free for as long as you live, providing a larger sum to draw upon later or to leave to your heirs. For those who don’t need to tap into their Roth IRA immediately in retirement, this allows for continued compounding without forced withdrawals.

Estate Planning Advantages

Roth IRAs are excellent estate planning tools. When you pass a Roth IRA to your beneficiaries (often non-spouse beneficiaries), they generally have to take distributions over a 10-year period, but these distributions are still tax-free. This allows your legacy to continue growing tax-free for a decade after your passing, providing a significant financial gift to your loved ones.

Future Tax Rate Uncertainty

With national debt and other economic factors, many financial experts predict that future tax rates could be higher than they are today. By contributing to a Roth IRA, you are essentially "pre-paying" your taxes now, locking in today’s tax rates on your contributions and potentially avoiding higher taxes on your earnings in the future. This acts as a hedge against future tax increases.

Planning Your 2026 Roth IRA Contributions

With the projected Roth IRA Limits 2026 in mind, it’s never too early to start planning your contributions. Here are some actionable steps:

1. Estimate Your 2026 MAGI

The first step is to get a realistic estimate of your Modified Adjusted Gross Income for 2026. This will determine if you qualify for direct Roth IRA contributions or if you’ll need to consider a backdoor Roth strategy. Factor in any anticipated salary increases, bonuses, or changes in income sources.

2. Maximize Your Contributions

Once you know your eligibility, aim to contribute the maximum amount allowed. Even if you can’t contribute the full amount at once, setting up automatic monthly contributions can help you reach the limit gradually throughout the year. For example, if the limit is $7,500, that’s $625 per month.

3. Consider the Backdoor Roth If Necessary

If your MAGI is too high for direct contributions, plan for the backdoor Roth strategy. This means ensuring you don’t hold any significant pre-tax Traditional IRA balances that would trigger the pro-rata rule. If you do, explore rolling those funds into an employer-sponsored plan before the end of 2025 or early 2026.

4. Review Employer-Sponsored Roth Options

Check if your employer offers a Roth 401(k) or Roth 403(b). If so, consider contributing to it, especially if you’re a high-income earner. The higher contribution limits make it an excellent complement to, or even alternative for, a Roth IRA.

5. Stay Updated on Official Announcements

Keep an eye out for the official IRS announcements regarding 2026 contribution limits and income thresholds, typically released in late October or November of 2025. This will confirm the exact figures and allow you to finalize your plans.

6. Consult a Financial Advisor

For complex financial situations or if you’re unsure about the best strategy for your specific circumstances, a qualified financial advisor can provide personalized guidance. They can help you navigate the intricacies of the Roth IRA Limits 2026 and integrate it into your overall financial plan.

Common Misconceptions About Roth IRAs

Despite their popularity, several misconceptions about Roth IRAs persist. Clearing these up can help you make more informed decisions about your retirement savings.

Misconception 1: "I can’t contribute to a Roth IRA if I have a 401(k)."

Reality: You can contribute to both a Roth IRA and a 401(k) (or Roth 401(k)) simultaneously, provided you meet the income eligibility requirements for the Roth IRA. These are separate types of retirement accounts with their own contribution limits.

Misconception 2: "Roth IRAs are only for young people."

Reality: While younger individuals benefit greatly from the long runway for tax-free growth, Roth IRAs can be beneficial at any age, even in retirement. The tax-free withdrawals and lack of RMDs for the original owner are attractive at any stage of life, provided you meet the income limits for contributions or utilize the backdoor strategy.

Misconception 3: "I lose money if I contribute to a Roth IRA instead of a Traditional IRA because I don’t get a tax deduction."

Reality: This is a common point of confusion. While you don’t get an upfront tax deduction with a Roth IRA, you gain tax-free withdrawals in retirement. The "better" option depends on whether you expect to be in a higher tax bracket now or in retirement. If you anticipate higher taxes in retirement, the Roth IRA is generally more advantageous. It’s a matter of when you pay your taxes, not if.

Misconception 4: "I can’t access my Roth IRA money until retirement."

Reality: As discussed, you can withdraw your contributions from a Roth IRA at any time, tax-free and penalty-free. This flexibility is a significant advantage. It’s only the earnings that are subject to a 5-year rule and age 59½ requirement for qualified tax-free withdrawals.

Conclusion: Maximizing Your Roth IRA in 2026

As we approach 2026, the Roth IRA continues to stand out as an indispensable tool for building a robust, tax-free retirement nest egg. Understanding the projected Roth IRA Limits 2026 – both contribution limits and income phase-out ranges – is the first step towards optimizing your retirement savings strategy. While the official numbers are yet to be released, planning based on informed projections allows you to be proactive.

Whether you’re eligible for direct contributions or need to employ strategies like the backdoor Roth IRA or leverage a Roth 401(k), the goal remains the same: harness the power of tax-free growth and withdrawals. By staying informed, estimating your MAGI, maximizing your contributions, and seeking professional advice when needed, you can ensure your Roth IRA plays a pivotal role in securing your financial future and enjoying a comfortable, tax-efficient retirement.

Don’t let the complexities deter you. The benefits of a Roth IRA are substantial and well worth the effort to understand and implement correctly. Start planning today to make the most of your Roth IRA Limits 2026 and build the retirement you envision.

& IRA")