Federal Retirement Benefits 2026: FERS vs. CSRS Analysis

As 2026 approaches, federal employees across the United States are increasingly turning their attention to a critical question: how do their federal retirement benefits stack up, and which plan offers the most value for their dedicated service? For many, understanding the nuances between the Federal Employees Retirement System (FERS) and the Civil Service Retirement System (CSRS) is not just an academic exercise; it’s a vital component of their long-term financial security. This comprehensive guide will delve deep into the intricacies of both systems, comparing their benefits, advantages, and potential pitfalls to help you determine which path could potentially offer up to 20% more value for your career.

The landscape of federal employment has evolved significantly over the decades, and with it, the retirement systems designed to support those who serve the nation. CSRS, established in 1920, represents an older, more traditional pension model, while FERS, introduced in 1987, is a more modern, three-tiered system that aligns more closely with private sector retirement plans. For employees nearing retirement, or even those just starting their federal careers, a thorough understanding of these systems is paramount. The decisions made today regarding contributions, investments, and retirement dates can have a profound impact on the quality of life in retirement.

Our goal is to provide a clear, actionable comparison of these federal retirement benefits for 2026. We will break down each system’s components, including annuities, the Thrift Savings Plan (TSP), Social Security, and healthcare considerations. By the end of this article, you will have a clearer picture of which system might provide a more robust financial foundation for your golden years, potentially unlocking significant additional value.

Understanding the Foundations: CSRS

The Civil Service Retirement System (CSRS) is a defined benefit plan that was the primary retirement system for most federal employees hired before January 1, 1984. It’s characterized by a generous annuity (pension) that is calculated based on an employee’s years of service and their ‘high-3’ average salary (the average of the highest three consecutive years of basic pay). Unlike FERS, CSRS employees do not pay into Social Security, and therefore, do not receive Social Security benefits based on their federal employment. This is a crucial distinction when comparing the overall value of the two systems.

CSRS Annuity Calculation: The Core Benefit

The CSRS annuity is the cornerstone of the system. It’s designed to provide a predictable, lifelong income stream. The formula for calculating the basic annuity is as follows:

- 1.5% of your high-3 average salary multiplied by the first 5 years of service.

- 1.75% of your high-3 average salary multiplied by the next 5 years of service.

- 2.0% of your high-3 average salary multiplied by all service years over 10.

For example, a CSRS employee with 30 years of service and a high-3 average salary of $100,000 would have their annuity calculated as: (1.5% x 5 x $100,000) + (1.75% x 5 x $100,000) + (2.0% x 20 x $100,000) = $7,500 + $8,750 + $40,000 = $56,250 per year. This provides a substantial, guaranteed income in retirement, which is a significant advantage for those under CSRS.

Cost-of-Living Adjustments (COLAs) in CSRS

Another attractive feature of CSRS is its annual Cost-of-Living Adjustments (COLAs). These adjustments are designed to help maintain the purchasing power of your annuity over time. CSRS COLAs are typically uncapped and are applied to the full annuity amount, often mirroring the Consumer Price Index (CPI). This can be a major factor in the long-term value of CSRS, especially during periods of higher inflation, as it helps to ensure that your retirement income keeps pace with rising living costs.

Healthcare and Life Insurance Under CSRS

CSRS retirees generally have access to the Federal Employees Health Benefits (FEHB) program and Federal Employees’ Group Life Insurance (FEGLI) at retirement, with the government often covering a significant portion of the premiums. While these are available to FERS employees as well, the specific contribution rates and retiree benefits can vary, making it important to compare the overall package.

Understanding the Foundations: FERS

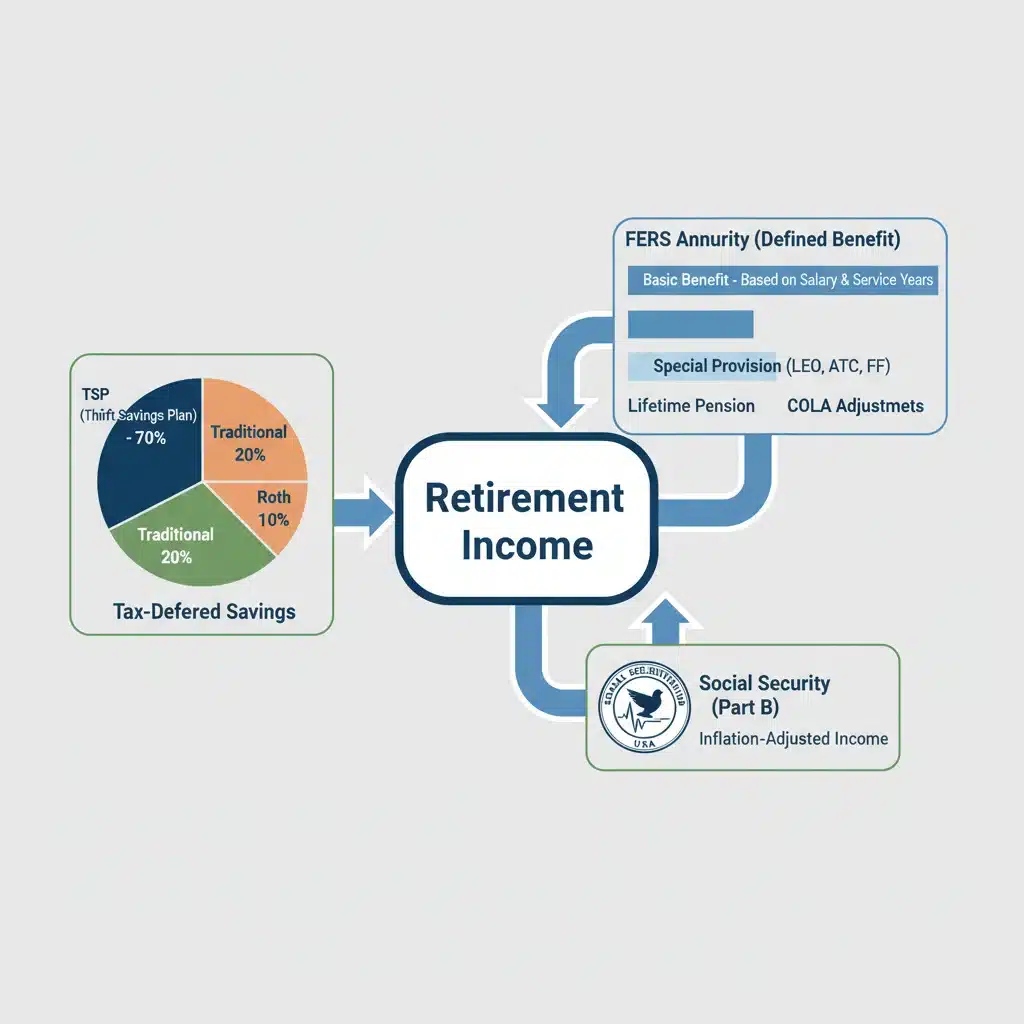

The Federal Employees Retirement System (FERS) is the retirement plan for federal employees hired on or after January 1, 1984, and for those who elected to switch from CSRS. FERS is a three-tiered system comprising:

- A Basic Benefit Plan (annuity)

- Social Security benefits

- The Thrift Savings Plan (TSP)

This multi-faceted approach aims to provide a more flexible and diversified retirement package, more akin to what is found in the private sector. The emphasis is on individual contribution and investment through the TSP, alongside a smaller defined benefit and the universal safety net of Social Security.

The FERS Basic Benefit Plan: A Smaller Annuity

The FERS Basic Benefit Plan is a defined benefit plan, similar to the CSRS annuity, but it is generally less generous. The annuity is calculated based on your years of service and your ‘high-3’ average salary. The standard formula is:

- 1.0% of your high-3 average salary multiplied by your years of creditable service.

For employees who retire at age 62 or later with at least 20 years of service, the multiplier increases slightly to 1.1%. Using the same example as before (30 years of service, high-3 average salary of $100,000), a FERS employee would receive: (1.0% x 30 x $100,000) = $30,000 per year. This is significantly less than the CSRS annuity, which is why the other two tiers of FERS are so critical to overall retirement security.

Cost-of-Living Adjustments (COLAs) in FERS

FERS COLAs are also generally less generous than CSRS COLAs. They are typically reduced during periods of higher inflation. For example, if the CPI increase is 2% or less, the FERS COLA will match it. If the CPI is between 2% and 3%, the FERS COLA will be 2%. If the CPI is greater than 3%, the FERS COLA will be one percentage point less than the CPI. This difference in COLA application can significantly impact the long-term purchasing power of a FERS annuity compared to a CSRS annuity.

The Thrift Savings Plan (TSP): A Powerful Investment Vehicle

The Thrift Savings Plan (TSP) is a defined contribution plan, similar to a 401(k) in the private sector. It is a critical component of FERS and where much of the potential for increased value lies. The TSP offers federal employees the opportunity to invest in a variety of funds, including G Fund (government securities), F Fund (fixed income), C Fund (common stock), S Fund (small-cap stock), I Fund (international stock), and Lifecycle (L) Funds, which are target-date funds. The significant advantage of TSP is the government’s contribution:

- Agency Automatic 1% Contribution: The government automatically contributes an amount equal to 1% of your basic pay to your TSP account, even if you don’t contribute yourself. This is essentially free money.

- Agency Matching Contributions: The government matches your contributions dollar-for-dollar for the first 3% of your basic pay, and 50 cents on the dollar for the next 2% of your basic pay. This means if you contribute 5% of your pay, the government contributes another 4%, totaling 9% of your salary going into your TSP account annually. This 5% contribution is crucial for maximizing your federal retirement benefits.

The power of compound interest and consistent contributions, especially with the government match, makes the TSP a formidable tool for building wealth for retirement. The growth potential of the TSP is often what allows FERS employees to achieve, and sometimes even surpass, the retirement income levels of their CSRS counterparts.

Social Security Benefits: A Universal Safety Net

Unlike CSRS employees, FERS employees pay into Social Security and are eligible for Social Security benefits upon retirement. This provides an additional layer of financial security and flexibility. Social Security benefits are calculated based on your highest 35 years of earnings, and the amount you receive depends on your earnings history and the age at which you claim benefits. For many FERS employees, Social Security represents a substantial portion of their overall federal retirement benefits, complementing their FERS annuity and TSP withdrawals.

Comparing Federal Retirement Benefits: FERS vs. CSRS in 2026

Now that we’ve outlined the individual components, let’s directly compare the two systems. The claim that one system offers ‘up to 20% more value’ is a bold one, and its validity depends heavily on individual circumstances, career length, contribution rates to TSP, and investment performance.

The ‘20% More Value’ Claim: A Deeper Dive

The idea of one system offering significantly more value often stems from the interplay of guaranteed benefits versus investment potential. CSRS offers a higher guaranteed annuity, which provides certainty. FERS, while having a smaller annuity, offers the significant growth potential of the TSP and the added layer of Social Security. For a FERS employee who consistently contributes at least 5% to their TSP throughout their career, benefiting from the full government match, and makes wise investment choices, the cumulative value of their TSP account at retirement can easily surpass the difference in annuity payments between FERS and CSRS.

Consider a scenario where a FERS employee consistently contributes 5% to their TSP for 30 years, and the TSP achieves an average annual return of 7%. The compound growth, combined with the government’s 4% matching contribution, can lead to a substantial retirement nest egg. This nest egg, when combined with the FERS annuity and Social Security, can indeed provide a higher overall retirement income than a CSRS annuity alone, especially when considering the flexibility of TSP withdrawals and potentially higher growth rates than inflation on the fixed CSRS annuity.

Key Differences at a Glance:

| Feature | CSRS | FERS |

|---|---|---|

| Primary Component | Generous Defined Benefit Annuity | Three-tiered: Basic Benefit, Social Security, TSP |

| Social Security | No (generally, for federal service) | Yes, employees pay into and receive benefits |

| Thrift Savings Plan (TSP) | Optional, no agency contributions/match | Automatic 1% + 4% matching contributions |

| Employee Contribution Rate | 7.0%, 7.5%, or 8.0% of basic pay | 0.8% (for FERS-RAE, FERS-FRAE) or 4.4% of basic pay, plus TSP contributions |

| Cost-of-Living Adjustments (COLAs) | Generally uncapped, full CPI | Reduced COLAs (capped or 1% less than CPI) |

| Survivor Benefits | Available, reduced annuity | Available, reduced annuity, plus Social Security survivor benefits |

Impact of Career Length and Salary

The length of your federal career and your high-3 average salary are critical factors for both systems. For CSRS, a longer career and higher salary directly translate to a significantly larger annuity. For FERS, while these factors also influence the basic annuity, their impact is amplified by the potential for greater TSP contributions and growth over a longer period. A FERS employee with a long career and consistent TSP contributions may see their total retirement package far exceed that of a CSRS counterpart, especially if market returns are favorable.

Maximizing Your Federal Retirement Benefits in 2026

Regardless of whether you are under CSRS or FERS, proactive planning is essential to maximize your federal retirement benefits. For FERS employees, the key lies in fully utilizing the TSP. For CSRS employees, understanding the intricacies of their annuity and exploring supplemental savings options is paramount.

For FERS Employees: Harnessing the Power of TSP

The single most impactful action a FERS employee can take is to contribute at least 5% of their salary to the TSP to receive the full government match. This is free money and significantly boosts your retirement savings. Beyond the match, consider increasing your contributions as your salary grows. The Roth TSP option, which allows for tax-free withdrawals in retirement, is another powerful tool to consider. Regularly review your TSP investment allocations to ensure they align with your risk tolerance and retirement timeline. Diversification across the various funds can help mitigate risk and maximize returns.

For CSRS Employees: Supplemental Savings and Strategic Planning

While CSRS offers a strong defined benefit, the lack of Social Security and government-matched TSP contributions means that supplemental savings are often crucial for a well-rounded retirement. CSRS employees should consider opening an Individual Retirement Account (IRA) or a private sector 401(k) if they have other employment. Understanding the CSRS annuity calculation and maximizing your high-3 average salary in the years leading up to retirement can also significantly increase your pension. Additionally, some CSRS employees may be eligible for a FERS Social Security supplement if they retire before age 62 and meet certain criteria, which is a complex but important aspect to investigate.

Healthcare in Retirement: A Universal Concern

Both CSRS and FERS retirees have access to the Federal Employees Health Benefits (FEHB) program, which is a significant advantage over many private sector retirement plans. However, healthcare costs in retirement can be substantial, and understanding your options is vital. Medicare generally becomes your primary insurer at age 65, and FEHB acts as a secondary payer. Planning for out-of-pocket expenses, prescription drug costs, and potential long-term care needs should be an integral part of your retirement strategy, regardless of your retirement system.

The Role of Financial Planning and Professional Advice

Navigating the complexities of federal retirement benefits can be challenging. This is where professional financial planning becomes invaluable. A financial advisor specializing in federal benefits can help you:

- Analyze your specific situation: They can run projections based on your years of service, salary, and contribution history for both FERS and CSRS.

- Optimize TSP investments: Provide guidance on asset allocation within your TSP to align with your retirement goals.

- Understand survivor benefits: Explain the implications of choosing survivor annuity options for your spouse.

- Integrate all income sources: Help you understand how your FERS annuity/CSRS annuity, Social Security, TSP, and any other savings will work together to create a comprehensive retirement income plan.

- Plan for taxes: Advise on the tax implications of withdrawals from TSP (traditional vs. Roth) and other retirement income.

- Address healthcare costs: Assist in planning for future healthcare expenses, including FEHB premiums and potential Medicare considerations.

For those under FERS, understanding how to maximize the TSP’s potential is often the key to unlocking that ‘up to 20% more value.’ For CSRS employees, understanding how to best supplement their robust annuity with other savings vehicles is crucial. The ‘20% more value’ isn’t an automatic outcome; it’s the result of informed decisions and diligent planning over the course of a career.

The Future of Federal Retirement Benefits

While this article focuses on the current structure for 2026, it’s important to acknowledge that federal retirement benefits are subject to legislative changes. Congress periodically reviews and proposes adjustments to both FERS and CSRS. Staying informed about potential changes through official OPM (Office of Personnel Management) communications and reputable federal employee news sources is always advisable. However, the fundamental structures of FERS and CSRS have remained relatively stable for decades, providing a solid foundation for your retirement planning.

Conclusion: Making Informed Choices for Your Golden Years

Comparing federal retirement benefits between FERS and CSRS for 2026 reveals two distinct paths to retirement security. CSRS offers a powerful, predictable defined benefit annuity with robust COLAs, but lacks Social Security and government-matched TSP contributions. FERS, on the other hand, provides a smaller annuity, but compensates with the substantial growth potential of the TSP (especially with agency contributions) and the universal safety net of Social Security.

The claim of ‘up to 20% more value’ for one plan over the other is not a universal truth but a potential outcome heavily influenced by individual choices, particularly for FERS employees who actively participate in and strategically manage their TSP. For a FERS employee who maximizes their TSP contributions and makes sound investment decisions, the combined value of their three-tiered system can indeed provide a more significant retirement income than a CSRS annuity alone, especially over a long career.

Ultimately, the ‘better’ system depends on your specific situation, risk tolerance, and engagement with your retirement planning. For both CSRS and FERS employees, the path to a secure and prosperous retirement in 2026 and beyond is paved with knowledge, proactive decision-making, and, often, the guidance of a qualified financial professional. Take the time to understand your benefits, make informed decisions, and secure the retirement you’ve earned through your dedicated federal service.