Federal Reserve Rate Hike 2026: 0.25% Impact & Market Analysis

Breaking: Latest Federal Reserve Interest Rate Decision for Early 2026 and Its 0.25% Immediate Market Impact

In a highly anticipated announcement that sent ripples through global financial markets, the Federal Reserve has confirmed a Federal Reserve Rate Hike of 0.25% for early 2026. This pivotal decision marks a significant moment in monetary policy, signaling the Fed’s ongoing commitment to navigating complex economic waters. The immediate market impact has been palpable, with investors, businesses, and consumers alike scrambling to understand and adapt to the new financial landscape.

For months, speculation has been rife regarding the Fed’s next move. Economic indicators, inflation trends, and employment figures have been under intense scrutiny, forming the backdrop against which this critical decision was made. This article delves deep into the implications of this Federal Reserve Rate Hike, exploring its immediate effects on various sectors, offering expert analysis, and providing insights into what lies ahead for the economy and your investments.

Understanding the Federal Reserve’s Decision: Why Now?

The Federal Reserve’s mandate is dual: to maximize employment and maintain price stability. These objectives often require a delicate balancing act, especially in dynamic economic environments. The decision to implement a 0.25% Federal Reserve Rate Hike in early 2026 was not made in a vacuum; it is the culmination of careful consideration of a multitude of economic factors.

Key Economic Indicators Influencing the Hike:

- Inflationary Pressures: Despite previous efforts, inflation may have remained stubbornly above the Fed’s target of 2%. Persistent supply chain disruptions, strong consumer demand, and geopolitical events could have continued to fuel price increases, necessitating a further tightening of monetary policy. The Fed aims to cool down an overheating economy without stifling growth entirely.

- Robust Labor Market: A strong and resilient labor market, characterized by low unemployment rates and rising wages, provides the Fed with the necessary room to maneuver. When employment is near its maximum sustainable level, the risk of a rate hike derailing job growth is reduced, allowing the Fed to focus more intensely on price stability.

- Economic Growth Trajectory: The overall health and growth trajectory of the economy play a crucial role. If the economy is demonstrating sustained, healthy growth, it can absorb a modest rate increase without significant adverse effects. The 0.25% Federal Reserve Rate Hike suggests the Fed believes the economy is robust enough to withstand higher borrowing costs.

- Global Economic Landscape: International economic conditions and central bank policies worldwide also influence the Fed’s decisions. A synchronized global effort to combat inflation, or conversely, divergent economic paths, can impact the effectiveness and necessity of domestic monetary policy adjustments.

The 0.25% increase, while seemingly small, sends a clear signal to markets about the Fed’s commitment to its long-term goals. It reinforces the central bank’s proactive stance in managing economic stability, even if it means confronting short-term market volatility.

Immediate Market Impact: A Snapshot

The announcement of the Federal Reserve Rate Hike immediately triggered responses across various financial markets. Understanding these initial reactions is crucial for investors and businesses.

Stock Market Volatility:

Typically, a rate hike can lead to initial declines in stock market indices. Higher interest rates increase borrowing costs for companies, which can impact their profitability and future earnings projections. Growth stocks, which often rely on future earnings potential, can be particularly sensitive to rising rates as their valuation models are more heavily discounted. However, the market’s reaction is not always uniform; some sectors might fare better than others.

Bond Market Adjustments:

The bond market is perhaps the most directly affected by interest rate changes. When the Fed raises rates, newly issued bonds typically offer higher yields, making existing lower-yield bonds less attractive. This can lead to a decrease in the price of existing bonds. The yield curve, which plots the yields of bonds across different maturities, often shifts in response to a Federal Reserve Rate Hike, with short-term yields typically rising more sharply than long-term yields.

Currency Fluctuations:

A rate hike in the U.S. generally makes the dollar more attractive to foreign investors seeking higher returns on their investments. This increased demand for the dollar can lead to its appreciation against other major currencies. A stronger dollar has implications for international trade, making U.S. exports more expensive and imports cheaper.

Commodity Prices:

Commodity markets can also react to a Federal Reserve Rate Hike. A stronger dollar can make dollar-denominated commodities, such as oil and gold, more expensive for holders of other currencies, potentially dampening demand and leading to price decreases. However, the impact varies significantly depending on the specific commodity and global supply-demand dynamics.

Expert Analysis and Future Projections

Financial analysts and economists are already dissecting the Fed’s decision, offering diverse perspectives on its long-term implications. The consensus often points to a period of adjustment, but the nuances of these predictions are vital.

Views on Inflation Control:

Many experts believe this Federal Reserve Rate Hike is a necessary step to bring inflation back to target levels. They argue that a proactive approach is better than allowing inflation to become entrenched, which could lead to more severe economic consequences down the line. However, some express concern that repeated hikes could tip the economy into a recession if not managed carefully.

Impact on Economic Growth:

The primary risk associated with a Federal Reserve Rate Hike is its potential to slow down economic growth. Higher borrowing costs can deter businesses from investing and expanding, and consumers from taking on new debt for large purchases like homes and cars. Analysts will be closely watching GDP growth figures in the coming quarters to assess the extent of this impact. The Fed’s challenge is to achieve a ‘soft landing’ – curbing inflation without triggering a significant downturn.

Potential for Further Hikes:

While this 0.25% hike is significant, the market will be looking for clues regarding the Fed’s future trajectory. Statements from Fed officials, meeting minutes, and future economic data will all be scrutinized for indications of whether more rate increases are on the horizon. The Fed’s data-dependent approach means that policy will remain flexible, adjusting to evolving economic realities.

Sector-Specific Implications:

- Technology and Growth Stocks: These sectors often face headwinds with rising rates due to their reliance on future earnings and debt financing.

- Financials: Banks and other financial institutions can sometimes benefit from higher interest rates as their net interest margins (the difference between what they earn on loans and pay on deposits) can widen.

- Real Estate: Higher mortgage rates can cool down the housing market, impacting both residential and commercial real estate sectors.

- Cyclical vs. Defensive Stocks: Defensive stocks (e.g., utilities, consumer staples) tend to perform better in uncertain economic times, while cyclical stocks (e.g., industrials, consumer discretionary) are more sensitive to economic cycles.

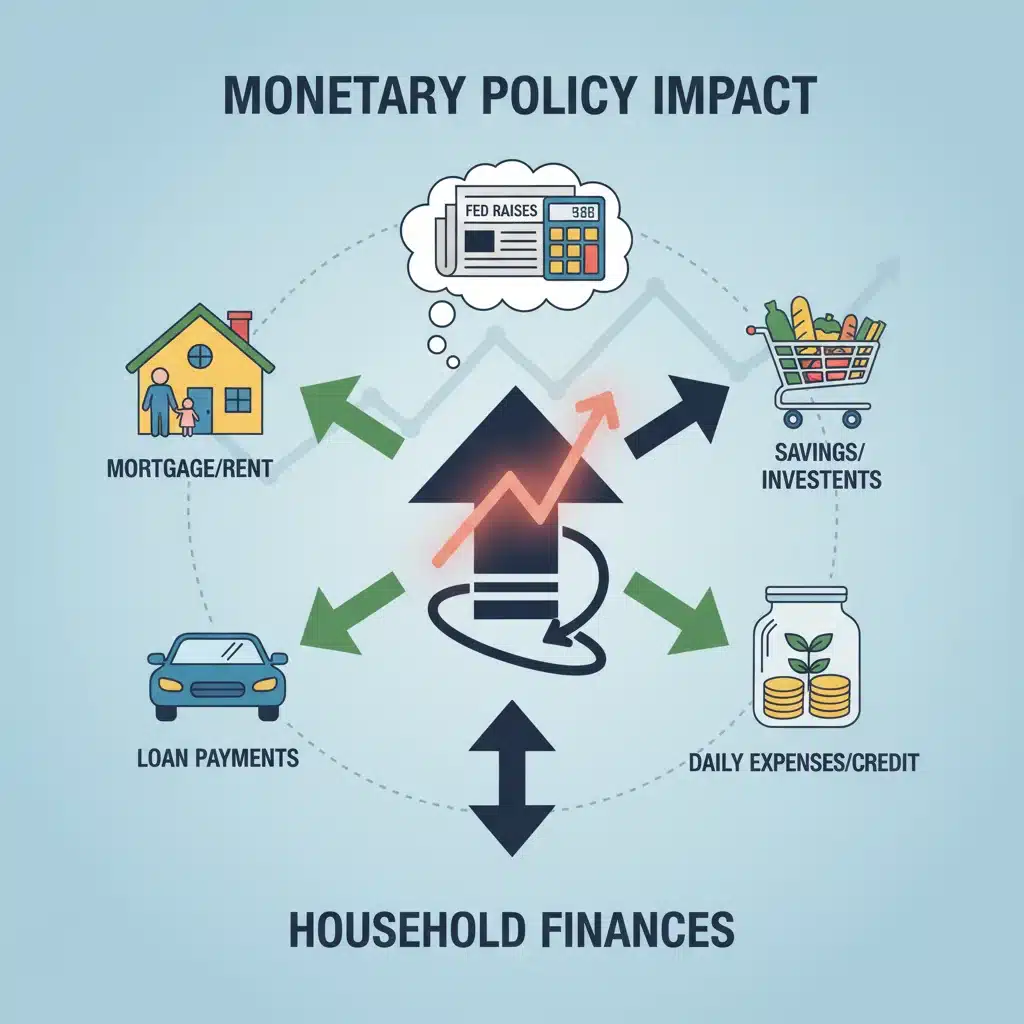

What This Means for You: Personal Finance and Investments

The Federal Reserve Rate Hike isn’t just an abstract economic event; it has tangible effects on your personal finances and investment strategies.

Borrowing Costs:

One of the most direct impacts is on borrowing costs. Expect to see an increase in interest rates for various types of loans:

- Mortgages: Both new fixed and adjustable-rate mortgages will likely become more expensive. If you are considering buying a home, this could impact your affordability.

- Credit Cards: Variable-rate credit cards will see their Annual Percentage Rates (APRs) increase, making it more costly to carry a balance.

- Auto Loans and Personal Loans: These will also likely experience an uptick in interest rates.

For those with existing variable-rate debt, the cost of servicing that debt will increase. It’s a good time to review your debt portfolio and consider strategies like debt consolidation or accelerating payments on high-interest loans.

Savings and Investments:

While borrowing becomes more expensive, savers might see some upside. Banks may offer slightly higher interest rates on savings accounts, money market accounts, and Certificates of Deposit (CDs). However, these increases are often modest and may still lag behind inflation.

For investors, the Federal Reserve Rate Hike necessitates a review of portfolios:

- Bonds: As discussed, existing bonds may lose value, but new bonds will offer higher yields. This could be an opportunity for investors seeking income.

- Stocks: A more selective approach to stock investing may be warranted. Companies with strong balance sheets, consistent earnings, and those less reliant on debt financing might be more resilient. Value stocks could potentially outperform growth stocks in this environment.

- Alternative Investments: Some investors might explore alternative assets that are less sensitive to interest rate fluctuations or offer inflation protection.

Retirement Planning:

For those nearing retirement, the impact of a Federal Reserve Rate Hike can be significant. Higher interest rates can reduce the value of bond portfolios, which are often a substantial component of retirement savings. However, they also offer opportunities for higher returns on new fixed-income investments. Diversification and a long-term perspective remain key.

Navigating the Economic Landscape: Strategies for Businesses

Businesses, from small enterprises to large corporations, must also adapt to the new economic reality shaped by the Federal Reserve Rate Hike.

Cost of Capital:

Higher interest rates directly increase the cost of capital for businesses. This affects everything from short-term operational loans to long-term financing for expansion projects. Businesses will need to re-evaluate their capital expenditure plans and potentially prioritize projects with higher expected returns.

Consumer Spending:

As consumers face higher borrowing costs and potentially slower wage growth in real terms, discretionary spending might decrease. Businesses reliant on consumer spending will need to adjust their sales forecasts and marketing strategies accordingly. Value propositions and essential goods and services may see more stable demand.

Supply Chain Management:

While the rate hike primarily addresses demand-side inflation, ongoing supply chain issues can still contribute to higher costs. Businesses that have successfully diversified their supply chains or invested in domestic production might be better positioned to mitigate these challenges, even as the Federal Reserve Rate Hike aims to cool economic activity.

Strategic Planning and Resilience:

In an environment of rising rates and potential economic slowdowns, businesses need to focus on financial resilience. This includes maintaining healthy cash reserves, optimizing operational efficiency, and carefully managing debt. Scenario planning for various economic outcomes becomes even more critical.

Historical Context: Lessons from Past Rate Hikes

Looking back at previous cycles of Federal Reserve Rate Hikes can offer valuable perspectives, though each economic period has its unique characteristics.

The 1970s and Early 1980s:

This era saw aggressive rate hikes by the Fed under Paul Volcker to combat rampant inflation. While successful in taming inflation, these policies also led to significant recessions. This period serves as a stark reminder of the trade-offs involved in monetary policy.

The Mid-2000s:

The Fed gradually raised rates from 2004 to 2006, aiming to cool down an overheating housing market and economy. While inflation remained relatively contained, the subsequent financial crisis highlighted the complexities of managing asset bubbles and interconnected financial systems.

Post-Financial Crisis and Post-Pandemic Eras:

More recently, the Fed has navigated periods of ultra-low rates to stimulate recovery, followed by gradual increases and then rapid hikes in response to post-pandemic inflation. These recent cycles underscore the Fed’s willingness to adapt quickly to unprecedented economic shifts.

The current 0.25% Federal Reserve Rate Hike for early 2026 should be viewed within this historical context. While the Fed aims to learn from the past, the present economic environment is always distinct, requiring tailored and flexible policy responses.

The Road Ahead: Monitoring Key Indicators

The impact of this Federal Reserve Rate Hike will unfold over time, and market participants will be closely monitoring several key indicators to gauge the effectiveness of the Fed’s policy and anticipate future moves:

- Inflation Data: Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) will be critical. A sustained decline towards the Fed’s 2% target would be a positive sign.

- Employment Reports: Non-farm payrolls, unemployment rates, and wage growth figures will indicate the health of the labor market and whether the economy is achieving a ‘soft landing’.

- GDP Growth: Quarterly GDP reports will show the overall pace of economic expansion or contraction.

- Consumer Confidence: Surveys on consumer sentiment can provide insights into future spending patterns.

- Business Investment: Data on capital expenditures and business sentiment will reflect corporate responses to higher borrowing costs.

- Global Economic Developments: International trade, geopolitical stability, and the policies of other central banks will continue to play a role.

The Federal Reserve’s communication will also be paramount. Statements from the Federal Open Market Committee (FOMC), press conferences by the Fed Chair, and minutes from meetings will offer valuable insights into the central bank’s thinking and future policy direction after this Federal Reserve Rate Hike.

Conclusion: Adapting to the New Monetary Landscape

The 0.25% Federal Reserve Rate Hike for early 2026 is a significant development, reflecting the central bank’s ongoing efforts to achieve its dual mandate of maximum employment and price stability. Its immediate impact has been felt across stock, bond, and currency markets, and its long-term effects will shape the economic trajectory for the coming years.

For individuals, this means a careful review of personal finances, especially regarding debt management and investment strategies. For businesses, it necessitates a focus on cost efficiency, strategic planning, and resilience in a potentially tighter credit environment. While the path ahead may involve adjustments and some uncertainty, understanding the rationale behind the Fed’s decision and its potential implications is the first step toward navigating this new monetary landscape successfully.

The market’s reaction, though initially volatile, will eventually settle as participants price in the new reality. The focus now shifts to how the economy absorbs this change and whether the Fed’s actions achieve the desired balance of cooling inflation without stifling growth. Staying informed and adaptable will be crucial for everyone in the months and years following this pivotal Federal Reserve Rate Hike.

")